A federal judge in Iowa has granted preliminary approval to a proposed class-action settlement to resolve accusations that Transamerica Life Insurance Co. improperly increased cost-of-insurance charges on certain life insurance policies in 2022 and 2023.

The agreement clears the way for policyholders to be notified and for a final approval hearing later this year. Although a court order issued by Chief U.S. District Judge C.J. Williams did not reveal the settlement amount, a website set up to manage the class action revealed that Transamerica will pay out $57 million.

The court certified a proposed settlement class that includes individuals and entities who currently own or previously owned certain life insurance policies during the defined class period.

The case, brought by the Estate of Lawrence Handorf and other plaintiffs, alleges disputes related to policy terms and costs. The settlement agreement, which is not opposed by Transamerica, would resolve all claims covered under the agreement if it receives final approval.

No wrongdoing assessed

Transamerica admits to no wrongdoing in the settlement. The insurer also agreed not to:

Impose any new additional cost-of-insurance rate or monthly deduction rate schedule increases on policies covered by the settlement for a period of five years, unless ordered to do so by a state regulatory body.

Cancel, void, rescind or deny a death claim submitted under the settlement class members’ policies or contest the validity of a policy based on an alleged lack of insurable interest or misrepresentation made in connection with the original application process under any applicable law or equitable principles.

The court said it is likely to find the settlement “fair, reasonable and adequate,” a key legal standard under federal rules governing class actions. The judge also determined that the case meets the requirements for class certification for settlement purposes.

As part of the order, the court appointed the plaintiffs as class representatives and named Susman Godfrey LLP as class counsel. A third-party administrator, Simpluris Inc., will oversee the notification process and handle requests from class members who wish to opt out or object to the settlement.

Class members have until May 30 to opt out of the settlement and retain their own right to sue Transamerica. Objections to the settlement must be received by the court by June 1, court documents say.

A final fairness hearing is scheduled for July 13, in Cedar Rapids, where the court will decide whether to grant final approval of the settlement, as well as rule on attorneys’ fees and other related matters.

The order also pauses all other proceedings in the case while the settlement process moves forward. If the settlement is not approved, the case would revert to its status prior to the agreement, and the parties would resume litigation.

While many insurance providers have begun adopting artificial intelligence, others are already racing ahead to the next stage of scaling solutions — a stage that could be marked by a trend of strategic partnerships, according to Jodie Wallis, global chief AI officer, Manulife.

Some insurance companies have been hesitant to adopt AI, due to concerns ranging from safety and security to governance concerns and more.

But not Manulife. The Canada-based parent company of John Hancock in the U.S. has taken a progressive approach to implementing AI, earning it global recognition as a life insurance leader in AI, and a top ranking for AI maturity in the Evident AI Index for Insurance.

Earlier this year, Manulife announced a new partnership with agentic AI platform Akka, just the latest of its advancements in technology. And Wallis believes this could be a trend the wider industry will start adopting.

“We believe this partnership is catching the attention of the wider insurance industry,” she told InsuranceNewsNet.

In her view, the “need to accelerate speed of deployments while maintaining or improving risk posture is a common challenge” for insurers seeking to scale their AI solutions, and strategic partnerships like this can help bridge that gap.

“The partnership reflects our need for engineering discipline and operational rigor as we scale AI in a highly regulated industry where trust, predictability and safety are essential,” Wallis said.

A new agentic AI emerges

Manulife plans to leverage Akka’s technology as it builds out an enterprise agentic AI platform, equipped with AI insurance agents capable of understanding tasks, analyzing information and acting.

“These agents support colleagues in areas such as underwriting, claims, customer service and investment research, helping them work faster and deliver more accurately. The platform reduces development time, lowers operational costs and ensures that every agent is built with strong governance, embedded safeguards and responsible AI controls,” Wallis said.

As the company develops this platform, which is currently in the beta testing phase, Wallis noted that heavy emphasis is being placed on systems that can operate with the “consistency, governance and compliance” needed to support both clients and colleagues across global markets.

However, she added that it was equally important to work with technology that complements Manulife’s Responsible AI philosophy — a set of published principles that support human agency and business conduct ethics.

“Responsible AI is embedded into every phase of our AI lifecycle, from design and development to deployment and ongoing monitoring. This partnership aligns directly with our Responsible AI Principles and reinforces our commitment to building AI systems that are explainable, resilient and safe,” Wallis said.

Key partnership strengths

Ethical synergy was just one of the reasons Manulife chose to partner with Akka, a digital platform that emerged in 2011 and has since racked up a notable list of clients across industries.

But the company’s strength in agentic AI and consistent results made it that much more appealing to one of the world’s largest insurers.

“Akka’s strength in orchestration, operational SLAs and system reliability is essential in a highly regulated industry,” Wallis explained. “Akka provides a durable, highly available runtime that strengthens the platform’s security, reliability and performance as AI becomes embedded in mission-critical workflows across the organization. They also enable a consistent developer experience across global markets.”

She noted that companies seeking to scale AI, like Manulife, stand to benefit from partnerships with companies or solutions that can enhance AI platforms and ensure systems can run reliably in a high-volume environment.

“By enabling AI agents at scale, we can accelerate decision-making, streamline complex processes and enhance customer experience across the enterprise. This is critical as we move from AI solutions that power better decisions to AI solutions that take action as part of our core operations,” Wallis explained.

Capitalizing on AI value

If all goes well with this partnership, Manulife hopes it will support the company’s goal of seeing over $1 billion in AI-driven gains over the next year alone.

And, according to Wallis, it’s not out of line with the strategic relationships Manulife has steadily announced over the years as part of its ongoing AI journey. She believes it builds on recent work with partners such as Adaptive ML, an AI software company, and its Adaptive Engine tool that supports reinforcement learning-based model optimization within Manulife’s AI platform.

In designing its AI platform, Wallis noted, Manulife set out to create an enterprise capability to “build, reuse and govern AI at scale” while avoiding multiple rounds of reinvention.

“The partnership supports our enterprise commitment to generating more than $1 billion in value from AI by 2027. Using Akka, AI practitioners get a head start with AI governance embedded for safety and consistency. Development can occur in parallel for local teams, and all that work is contributed back to be reused by others,” she said.

Something significant is happening in the life insurance market, and it is unfolding quietly, one kitchen table conversation at a time. Clients who purchased whole life or universal life policies in the 1980s, 1990s and early 2000s are now in or approaching retirement. Many of them face a reality they did not anticipate: the cost of living is higher than they planned for, retirement income is stretched and they are actively looking for ways to generate liquidity.

Mike Mathweg

What most of these clients do not know is that the policy sitting in their file drawer may represent a significant financial resource. Life settlements, 1035 exchanges, and accelerated death benefits are powerful, consistently underused tools that can convert an existing policy into immediate value. As their agent, you are the only professional positioned to introduce these options. If you are not doing so proactively, you leave both your clients and your practice underserved.

When the life insurance policy itself becomes the asset

When a client decides they no longer need or can afford their life insurance policy, the conversation does not have to end with a surrender. Most policyholders, and many agents, do not realize a secondary market exists specifically to purchase those policies for significantly more than the insurance carrier will ever offer as a cash surrender value. That market is the life settlement industry, and it represents one of the most underused opportunities in an agent’s practice today.

A life settlement allows a policyholder to sell their life insurance policy to a third-party buyer in exchange for a lump sum cash payment. That payment is determined by several factors – including the insured’s age, health status, policy face amount and premium obligations – but in most cases it exceeds what the carrier would pay to surrender the policy outright. For clients who have been holding onto a policy they no longer want, that difference can be substantial.

For agents, the opportunity is twofold. First, facilitating a life settlement is a commissionable transaction. Instead of watching a policy walk out the door with no benefit to anyone, the agent earns compensation for connecting the client with a solution that delivers real value. Second, and perhaps more important, the client now has a meaningful sum of cash in hand. That is not the end of the conversation. That is the beginning of the next one.

As the trusted advisor who surfaced this opportunity, you are perfectly positioned to help that client put their money to work. Whether the conversation leads to an annuity, a new investment vehicle or a restructured protection strategy, there is a second commission opportunity built directly into the outcome of the first. One policy, two commissions, and a client who now sees you as the professional who found money they did not know they had.

Repositioning cash value without the tax consequences

A 1035 exchange allows a policyholder to transfer the cash value of a life insurance policy directly into an annuity, a long-term care insurance policy or a new life insurance policy without triggering a taxable event. For clients who have accumulated meaningful cash value in an older policy but would benefit more from guaranteed income or long-term care protection, this is one of the most efficient repositioning tools in the business.

This conversation is most relevant when a client has a policy with real cash value but diminishing need for the original death benefit. It is particularly powerful for clients who are concerned about long-term care costs and want to use existing assets rather than out-of-pocket premiums to fund that coverage. An exchange into a hybrid life and long-term care product can address both concerns in a single, tax-efficient transaction.

Ask your client when they last reviewed whether their current policy structure still matches their retirement income goals. Most clients assume their policy is static. Introducing the idea that the cash value inside that policy can be repositioned without a tax event opens a door that most agents never walk through.

The living benefit they already own

Many life insurance policies issued in the last two decades include accelerated death benefit riders that allow policyholders to access a portion of the death benefit while still living if they are diagnosed with a terminal, chronic or critical illness. This feature is consistently overlooked, and in many cases, clients have no idea it exists within their policy.

When a client is facing a serious health diagnosis and needs liquidity to cover medical expenses, in-home care or other costs associated with declining health, this option deserves to be on the table immediately. Unlike a life settlement, the client does not sell the policy. They are simply accessing a benefit they have already paid for.

Make it standard practice during every annual policy review to walk clients through every rider attached to their coverage. Many clients have never read their policy in full. When you explain that their policy may already contain a living benefit provision, the reaction is almost always the same: genuine surprise, followed by gratitude. That moment builds the kind of trust that no marketing campaign can replicate.

The conversation starts with you

Your clients will not come to you asking about life settlements, 1035 exchanges, or accelerated death benefits. They do not know these options exist, and even if they have heard the terms, they almost certainly do not understand how to apply them to their specific situation. That is exactly why the conversation must come from you.

The clients who need these conversations most are the ones you have known the longest. They are the policyholders who trusted you with a purchase decision decades ago and who now face a retirement landscape that looks nothing like what they planned for. Revisiting those policies today, with fresh eyes and a broader set of tools, is not just good practice. It is what they hired you to do.

Pull your client list. Start with everyone over 60 who holds a permanent life policy. Pick up the phone. The agents having these conversations right now are the ones whose clients will never leave.

MONTPELIER, Vt.–(BUSINESS WIRE)– National Life Group recently named Jason Doiron Chief Executive Officer of its investment affiliate, NLG Capital, as the organization continues to focus on strategic growth. Doiron is also Executive Vice President and Chief Investment Officer of National Life Group.

Jason Doiron, Chief Executive Officer of NLG Capital

As CEO of NLG Capital, Doiron will be responsible for supporting the ongoing growth of the overall organization. As CIO, he sets the investment strategy and asset allocations for National Life Group’s investment portfolios.

“Jason is an innovative leader whose deep investment expertise has helped position National Life Group among the top 10 life insurance companies*,” said Chair, CEO, and President Mehran Assadi. “His commitment to the business and proven track record of accelerating growth in volatile markets are exceptional. He is well positioned to succeed as CEO of NLG Capital.”

Doiron was named Chief Investment Officer of National Life Group in 2016. As CIO, he led the build-out of NLG Capital into an industry-leading proprietary asset management platform, overseeing the expansion of the investment team and the opening of the firm’s New York City office. During his tenure as CIO, National Life Group’s assets have grown from less than $20 billion in 2016 to more than $65 billion today, with NLG Capital serving as a key driver of the organization’s competitive edge.

Doiron joined National Life Group in 2008 as Head of Derivatives and was named Portfolio Manager of the General Account and Head of Fixed Income in 2010. He subsequently took on portfolio management responsibilities across several Sentinel mutual funds before being appointed Head of Investments for Sentinel — National Life Group’s wholly owned asset management subsidiary — in 2013, a role he held through Sentinel’s sale in 2018.

Earlier in his career, Doiron was Director of Quantitative Trading – U.S. Debt Markets for the Royal Bank of Canada’s Capital Markets group, and prior to that held a position with Citigroup Global Investments.

Doiron earned an MBA from the University of Chicago Graduate School of Business and a BA from the University of Maine at Farmington. He holds both the Financial Risk Manager (FRM) and Professional Risk Manager (PRM) designations.

About National Life Group

National Life Group has been keeping promises since 1848, providing access to flexible, secure life insurance and annuities for families, businesses, educators, and first responders nationwide. With an independent, entrepreneurial spirit, our values are to “Do good, Be good, Make good” for our customers, agents, employees, and the communities we serve. Learn more at NationalLife.com.

National Life Group® is a trade name of National Life Insurance Company (NLIC), Montpelier, VT founded in 1848, Life Insurance Company of the Southwest (LSW), Addison, TX chartered in 1955, and its affiliates. Each company is solely responsible for its own financial condition and contractual obligations. LSW is not an authorized insurer in New York and does not conduct insurance business in New York. NLIC, the flagship of National Life Group was founded in 1848, and all references to 1848 are attributable to NLIC.

Products are issued by National Life Insurance Company and Life Insurance Company of the Southwest.

NLG Capital is the registered investment advisor affiliate of National Life Group responsible for managing the organization’s investment portfolios.

Life and annuity carrier executives are concerned about a critical issue – the increasing cost of customer acquisition, driven in part by the commission structure of products sold through third-party distribution. A heavy reliance on TPD is unavoidable – career agency/captive agent models have continued to lose overall market share. And the DTC channel has not reached a level of maturity to achieve a significant premium for most carriers.

Chris Taylor

But carriers also need to solve for cost – significant commission costs put pressure on the carrier to maintain lower lapse rates for long-term profitability. But without truly “owning” the customer relationship, persistency can be difficult.

Carriers have historically managed persistency in five ways:

Persistency-based incentive compensation

Predictive analytics and data-driven (e.g., lapse models)

Product design and features

Automated payment facilitation and communications

Underwriting and suitability standards

But managing lapses addresses the long-term profitability of the customer, not the cost of acquiring the customer.

To address the cost, carriers need a new strategy – a DTC/advisor hybrid channel.

Reimagining the purchase journey

The DTC channel has historically struggled as a serious channel for a variety of reasons – product complexity, lack of advisor touch, poor sales tools, etc. This has caused many carriers to retreat from the DTC channel.

But consumer behavior has shifted decisively toward digital. According to the 2025 LIMRA/Life Happens Insurance Barometer Study, 92% of consumers now research life insurance online (up from 71% a decade ago), yet only 25% are ready to complete the entire purchase DTC. The remaining 75% explicitly want professional guidance at key decision points. This creates the perfect conditions for a customer-opt-in hybrid model that maximizes low-cost digital volume while delivering high-intent leads to advisors.

Two key insights for carriers:

Some customers are ready for a purely digital insurance purchase experience.

A digital-first sales process can provide a strong lead program for advisors.

For carriers, this means designing a process that begins with education and strong digital sales tools across all products. Carriers should design this purchase experience to allow a customer to opt into a direct purchase. That is the best-case scenario for a carrier – no commission paid and an accelerated path to profitability.

More important is the customer’s ability to off-ramp from the digital-first experience and move to a financial advisor at any point. A key decision for carriers is what level of purchase experience the carrier wants to provide – this could range from a full purchase experience across all products to developing only a qualified lead program.

Addressing carrier concerns

One common carrier concern is lead leakage: What happens if an advisor receives the warm lead and ultimately places the business with a competing carrier? Industry data shows this risk is already baked into third-party distribution — advisors typically place only 49%-54% of life insurance with their primary carrier. The DTC/agent hybrid improves the carrier’s position: it can dramatically lower overall acquisition cost (replacing 80% or more of first-year commissions with modest lead fees or shared compensation). Carriers that feed advisors high-quality, context-rich leads consistently report stronger long-term partner relationships and improved wallet share over time.

What it takes for carriers to win

For L/A carriers interested in developing this program, execution remains everything, but there are clear requirements for success:

World-class end-to-end DTC platform — Intuitive user experience, simplified product variants for self-serve, AI-assisted underwriting and real-time issuance capabilities

Intelligent, non-intrusive opt-in prompts — Triggered by user behavior (e.g., time on complex pages, repeated questions or quote review) with clear value propositions

Seamless, context-rich advisor handoff — Prepopulated applications, shared digital session and advisor dashboards so the warm lead feels effortless.

Balanced compensation and incentives — Tiered structures that reward DTC volume for the carrier while giving agents attractive economics on opted-in leads

Robust analytics and testing — Predictive models to flag when a prospect might benefit from advisor help

Strong compliance and suitability framework — Clear consent flows, audit trails and product guardrails to avoid mis-selling risks on either path

Targeted marketing + pilot approach — Focus on segments most likely to self-serve or benefit from choice; start with simpler products before expanding to full life/annuity suites.

Distribution partner alignment — Transparent communication that this platform augments their business with higher-quality, lower-effort leads.

Carriers that nail the digital foundation and behavioral nudges can achieve lower acquisition costs, higher customer satisfaction and a scalable model that works for both self-directed buyers and those who value advice. This doesn’t replace persistency/lapse management. Indeed, the combination of reduced acquisition costs and a focus on persistency improves the entire economics.

This is a significant investment, but shifting digital expectations, particularly for younger generations, will force carriers to embrace this new age.

Since the 2020 pandemic, life insurance sales have surged. In 2025, policy counts jumped 7% year over year, but there remains work to be done, LIMRA researchers say.

“Despite these record sales, we haven’t seen a meaningful decline in the life insurance needs gap,” Bryan Hodgens, head of LIMRA research, said during a recent LinkedIn Live titled, “Understanding the Elusive Life Insurance Consumer.”

Hodgens was joined by Steve Wood, research director for LIMRA’s Markets Research, to discuss results from the 2026 Insurance Barometer Study, conducted jointly by nonprofit industry trade associations LIMRA and Life Happens.

“When the pandemic hit in 2020, we saw a fairly significant rise in the people who said they don’t have life insurance and need to buy some or they have some and need more,” Wood said.

Wood said the pandemic led to a rise in awareness of the need for life insurance, as there was a lot of premature mortality. Despite better health outcomes and vaccines, that awareness stayed elevated for five or six years, but it started dropping last year.

Since LIMRA, along with some of its member companies, has been in business for over 100 years, researchers were able to look back to 1918 and compare the rise in interest in life insurance following the influenza pandemic in that year.

“It matches almost perfectly what we saw from the 2020 pandemic. It’s about a four-year tail in interest in life insurance following a global pandemic,” Wood said.

During the LinkedIn Live, they discussed the many factors impacting life insurance sales, including demographics, technology advances, changes in distribution and overestimating the cost.

“By 2030, there will be more people over 65 than under 30,” Hodgens said, noting that the advisor population is also aging.

At the same time, Wood notes that younger generations are delaying or rejecting entirely life events like marriage or starting a family. “We know that’s a huge driver in first-time life insurance purchasing,” Wood said.

‘Personal connections’ are key

Additionally, the industry is using artificial intelligence and other new technologies to streamline the digital process, underwriting, and the speed to market.

“All of these technological advancements are helping more people understand life insurance in a simpler, faster way,” Wood said. “That is allowing our human agents to make those personal connections, which ultimately is what drives sales of more life insurance.”

This is important because the 2026 Insurance Barometer study revealed that 40% of Americans have little or no understanding of life insurance.

“People don’t buy what they don’t understand,” Wood noted. “So how do we get them to understand what life insurance is, how it works and how it’s really different from health insurance or property and casualty insurance?”

Another potential barrier to some people getting life insurance may be a misunderstanding of the cost of life insurance.

In the most-recent Barometer study, instead of just asking them about one particular policy, the study asked respondents about themselves and how much a very basic $250,000 level term, 20-year policy would be for them.

They were asked to rate their health on a scale of one to 10, and then LIMRA developed a matrix pricing for that person.

“What we find probably isn’t surprising, but essentially the younger and healthier a person is, the more they overestimate – often by as much as 10 times the actual cost – what that policy would be for them,” Wood said.

Wood said that younger people think life insurance is as much as $1,200 a year when, in fact, the younger and healthy you are, the cheaper it is to buy life insurance.

Entire contents copyright 2026 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Ann Moran Heiss, age 96, of Danvers and formerly of Dalton and Pittsfield, Massachusetts, passed away peacefully on April 27, 2026. Ann was born on Long Island, New York, the beloved daughter of Edward and Martha Moran, and the cherished sister of her late brothers, Edward and John.

The sudden passing of her father at age 42 required Ann to enter the workforce immediately after graduating from Lynbrook High School, rather than pursuing her plans for college. In 1952, while working as a secretary in New York City, she was introduced to her future husband, Everett Heiss, of Queens Village, New York. They were married in 1954, lived briefly in Detroit, Michigan, and then settled in the Berkshires when Everett began his career with Berkshire Life Insurance Company in Pittsfield. They raised their three children in nearby Dalton and later moved to Pittsfield.

Ann was a devoted mother, a Camp Fire Girls leader, and a communicant of St. Agnes Church in Dalton. Once her children were in school full-time, she began working as a teacher’s aide at Dalton Junior High School. Approaching the age of 40, she made the decision to pursue her long-held dream of higher education. She graduated 1930-2026

from Berkshire Community College and later North Adams State College with honors, earning her teaching degree. Ann went on to work in the Pittsfield and Cheshire school systems as a Reading Specialist. In later years, she also obtained her real estate license, assisting clients and friends throughout the Berkshires.

Ann was known for her great sense of humor and her generous, kind heart. She rooted for the underdog, was quick to laugh, and took joy in writing thoughtful notes to those she loved. She and Everett shared a love of music and dancing, especially as members of the Votre Soirée dance group, where they gathered monthly with close friends. They also enjoyed traveling throughout the US in their RV, exploring several national parks.

Ann’s compassion was evident in her actions—whether bringing gifts to a family displaced by a Christmas house fire, volunteering at a hospital gift shop, or helping Spanish-speaking workers adjust to new jobs by assisting with English. She was an active member of the philanthropic educational organization P.E.O., supporting women in their pursuit of education.

Ann and Everett built a life rich in friendship and community, both in the Berkshires and in Florida, where they spent 26 winters. Together, they celebrated more than 71 years of marriage.

Ann is survived by her devoted husband, Everett; her beloved children and their spouses: Barbara (Robert Goodwill), Susan McDermott (Robert), and Brian (Sydney); her grandchildren and their spouses, Sara McDermott (Jon McManus), Jeff McDermott (Kristen), Emily Heiss, and Anna Heiss; and her two great-grandchildren, Annie and Claire McDermott, as well as many nieces and nephews.

She will be deeply missed by all who knew and loved her.

FUNERAL NOTICE: A liturgy of Christian Burial will be held Tuesday May 5, 2026 at 11 am at St. Agnes Church, Main Street Dalton, celebrated by Rev. Brian Mc-Grath. Burial will follow in Pittsfield Cemetery. Receiving hour will be held at the church beginning at 10:15.

In lieu of flowers, memorial donations may be made in her name to: Care Dimensions of Danvers c/o Dery Funeral Home 54 Bradford St. Pittsfield MA 01201

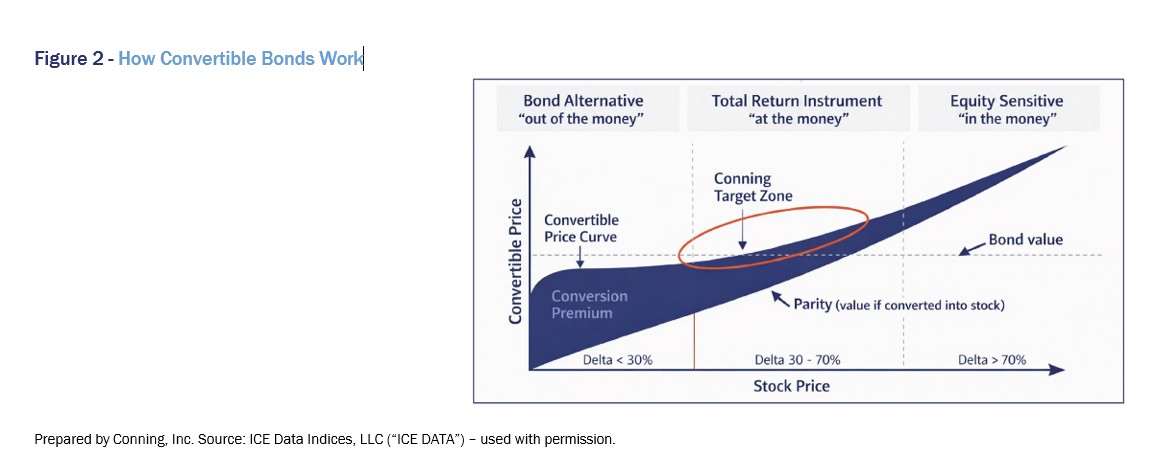

The convertible market has grown significantly in recent years, reflecting increased equity issuance and evolving corporate financing needs. As hybrid securities combining bond and equity characteristics, convertibles have historically delivered risk and return characteristics between equities and fixed income.

David A. Tyson

For insurers, convertibles may offer a way to enhance return potential while maintaining downside protection through the bond component. Credit quality, equity sensitivity and market composition remain key considerations for portfolio construction. As issuance expands and market conditions evolve, convertibles may play an increasing role in diversified insurance portfolios.

Andrew Willard

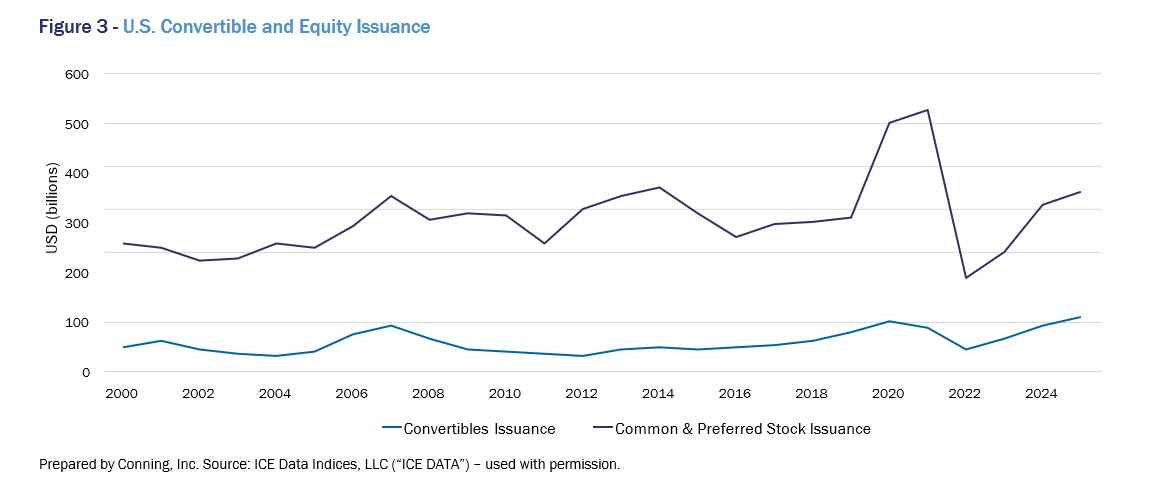

The convertible market has experienced a notable shift in issuance trends in recent years. Following a period of subdued issuance after the global financial crisis, activity increased significantly beginning in 2020. Issuance accelerated in 2020 and 2021 and has remained elevated, with 2024 and 2025 representing particularly strong years.

Structural characteristics of convertibles

Convertible securities combine features of both bonds and equities. The majority are structured as bonds, with a smaller portion issued as preferred stock.

A key characteristic of convertibles is the presence of a bond value, which provides a floor supported by maturity and coupon payments. Over time, the relative importance of coupon income has declined, with bond floor protection increasingly driven by maturity value.

In addition to bond features, convertibles include an embedded option that allows participation in equity upside. As the underlying stock price increases, the value of the convertible rises accordingly.

However, as convertibles move further into equity-sensitive territory, their value converges toward equity value. Companies often call convertibles to encourage conversion into equity, particularly when the underlying stock performs well.

As equity prices decline, the bond component becomes more prominent, though increasing credit risk must be considered. This dynamic highlights the importance of credit analysis, particularly in lower price scenarios.

Issuance trends and market drivers

Convertible issuance has historically been closely correlated with equity issuance, with increases in equity issuance typically accompanied by higher convertible issuance.

Periods such as 2007 illustrate this relationship, when both equity and convertible issuance increased. At that time, a significant portion of issuance came from the financial sector, contributing to elevated exposure within convertible indices before the market dislocation in 2008.

Following the global financial crisis, both equity issuance and the number of publicly listed companies declined, contributing to a decline in convertible issuance throughout much of the 2010s.

In contrast, corporate bond issuance has continued to grow over time. However, when evaluated relative to overall equity market value, the market value of outstanding debt has not increased as a percentage of equity market value. This dynamic reflects the influence of rising equity market valuations, which have supported increased debt issuance capacity in capital markets.

Convertible issuance is not primarily driven by companies attempting to time the market. Rather, it is influenced by financing needs and the ability to access various sources of financing. As a result, issuance patterns reflect broader market conditions rather than tactical decision-making.

Convertibles as a financing tool

Convertibles function primarily as an equity-oriented financing instrument. Companies use them to raise capital for a variety of purposes, including funding growth initiatives, supporting balance sheets or maintaining credit ratings.

The events of 2020 illustrate this dynamic. During the pandemic, many companies faced increased financing needs. Convertible issuance increased significantly, reaching approximately $100 billion, as companies accessed both equity and convertible markets.

In some cases, convertibles were used alongside equity issuance to raise substantial capital. For example, companies seeking to preserve credit quality or maintain liquidity issued convertibles as part of broader capital-raising efforts.

Convertible issuance also reflects a company’s life cycle dynamic. Early-stage companies typically rely on bank financing before accessing public markets through an initial public stock offering. Following this transition, convertibles often represent an initial form of public market debt issuance, as traditional bond investors are less willing to invest in smaller or less diversified companies.

As a result, the convertible market includes a significant proportion of smaller or unrated issuers, reflecting its role in bridging equity and debt financing.

Convertible segments and return sensitivity

Convertibles can be broadly categorized based on their sensitivity to the underlying equity:

• Out-of-the-money (bond alternatives):

Securities where the stock price is well below the conversion price, behaving more like bonds.

• At-the-money (balanced exposure):

Securities where bond and equity values are closely aligned. These typically exhibit moderate equity sensitivity and are often the focus of portfolio allocation.

• In-the-money (equity-sensitive):

Securities with significant equity exposure, often trading at higher prices and demonstrating stronger sensitivity to stock movements.

Most new issues are in the “at-the-money” segment, which typically offers the highest balance between bond protection and equity participation (and is often the primary focus for our portfolio construction.) As the underlying stock moves over time, the convertibles then move into the in-the-money category if the stock does well or if the stock falls, the convertible falls into the out-of-the money category. Ongoing portfolio management keeps the overall portfolio’s risk profile in line with objectives.

Market composition and credit considerations

The convertible market includes a large proportion of unrated securities, with typically 75-80% of the universe falling into this category. This reflects the presence of smaller or earlier-stage companies.

Despite this composition, higher-quality opportunities exist within the market, including many issuers that exhibit characteristics consistent with investment-grade or near-investment-grade profiles.

Portfolio construction for insurers often emphasizes higher-quality issuers to preserve downside protection through the bond component of convertibles. Credit analysis remains a critical component in evaluating risk, particularly when equity prices decline and credit exposure becomes more important.

Return characteristics and benchmark behavior

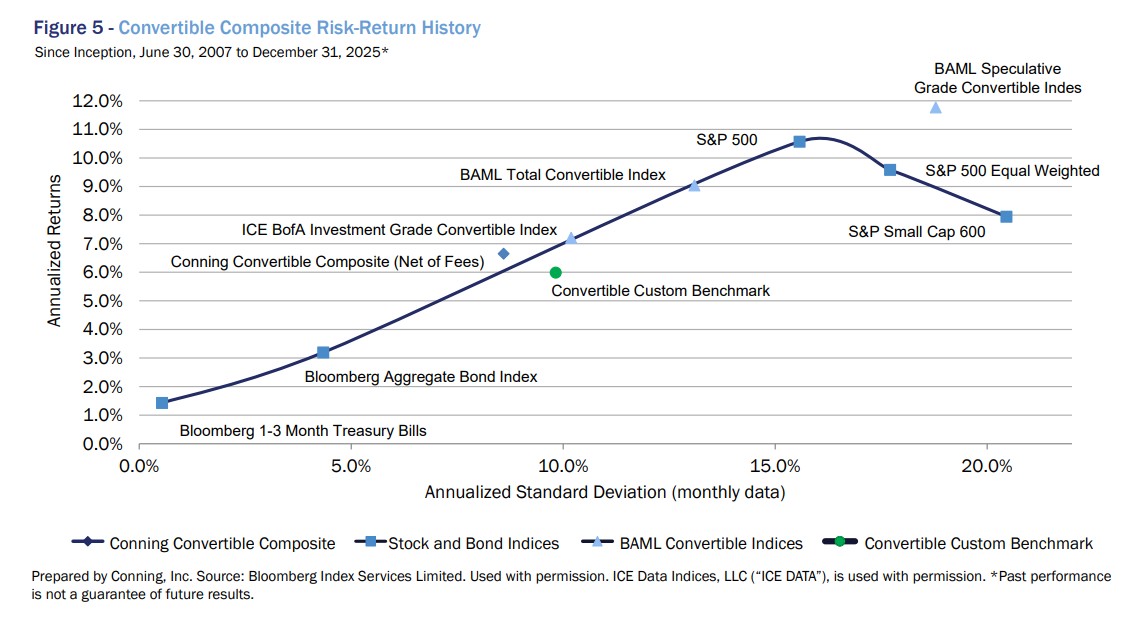

Convertible returns have historically been positioned between equity and fixed income markets. Performance observations indicate that returns have been generated between the S&P 500 and the Bloomberg Aggregate Bond Index.

While shorter-term performance may deviate, particularly during periods when equity market performance is dominated by a small number of companies, longer-term outcomes have aligned with the objective of delivering risk and return characteristics between stocks and bonds.

Different segments of the convertible market exhibit varying levels of risk. Speculative-grade convertibles tend to demonstrate higher volatility, while investment-grade convertibles typically align more closely with a balanced risk profile between equities and bonds.

Portfolio positioning and strategy considerations

Portfolio construction within convertibles involves balancing credit quality and equity sensitivity. Emphasis is often placed on maintaining exposure within the intermediate “at-the-money” range, where the trade-off between risk and return is most balanced.

Portfolio and benchmark allocations shift as market conditions evolve, with issuance patterns and equity performance influencing portfolio exposures.

Differences between portfolio positioning and benchmark composition can result in tracking variation, reflecting the range of approaches available in managing convertible portfolios.

Why this matters for insurers

For insurers, convertible securities offer a way to balance return objectives with downside protection. In environments where equity valuations are elevated or fixed income returns are constrained, convertibles can provide partial equity participation while maintaining the defensive characteristics of bonds. Portfolio allocations can focus on higher-quality issuers and at-the-money securities to balance credit risk and equity sensitivity. Convertibles serve as a complementary allocation within surplus or total return portfolios, particularly for insurers seeking diversification and intermediate risk exposure between equities and traditional fixed income.

Convertible issuance has increased significantly in recent years, reflecting stronger equity market conditions and corporate financing needs. As a hybrid instrument, convertibles continue to serve as a bridge between equity and debt markets, with issuance patterns closely aligned with equity activity.

The structural characteristics of convertibles support return outcomes between equities and fixed income, consistent with their role in portfolio construction.

For insurers, convertibles offer a flexible asset class that can be positioned to balance downside protection and equity participation, with outcomes dependent on credit quality, market conditions, and portfolio allocation decisions.

As insurers continue to evaluate portfolio resilience, return generation, and diversification, convertibles may represent a useful tool within a broader portfolio strategy. Their hybrid characteristics allow insurers to participate in equity upside while maintaining elements of downside protection, making them particularly relevant in environments where balancing risk and return remains a key objective.

David A. Tyson, Ph.D., CFA, is a managing director and portfolio manager at Conning. Contact him at david.tyson@innfeedback.com.

Andrew Willard is an assistant vice president for equity strategies on Conning’s portfolio management team. Contact him at andrew.willard@innfeedback.com.