SINGAPORE–(BUSINESS WIRE)– AM Best has affirmed the Financial Strength Rating of A- (Excellent), the Long-Term Issuer Credit Rating of “a-” (Excellent) and the Vietnam National Scale Rating of aaa.VN (Exceptional) of PVI Insurance Corporation (PVI Insurance). The outlook of these Credit Ratings (ratings) is stable.

The ratings reflect PVI Insurance’s balance sheet strength, which AM Best assesses as very strong, as well as its strong operating performance, neutral business profile and appropriate enterprise risk management. The ratings also factor in rating enhancement from PVI Insurance’s ultimate parent, HDI Haftpflichtverband der Deutschen Industrie V.a.G. (HDI V.a.G.).

PVI Insurance’s balance sheet strength is underpinned by its risk-adjusted capitalisation, as measured by Best’s Capital Adequacy Ratio (BCAR), which is expected to remain at the strongest level over the medium term. PVI Insurance benefits from good financial flexibility, given its majority ownership by HDI V.a.G. AM Best views the company’s investment portfolio to be of moderate risk, with investments mostly allocated toward cash and term deposits and the remainder held in non-rated corporate bonds, affiliated private equity investments and real estate. Offsetting factors include the company’s high dividend payout ratio and high reinsurance dependence to support the underwriting of large commercial property, engineering and energy risks.

AM Best assesses PVI Insurance’s operating performance as strong, supported by the company’s five-year average return-on-equity ratio of 16.7% (fiscal year [FY] 2021-FY 2025). Operating earnings improved in FY 2025, supported by an improvement in loss experience and favourable reserve development relating to Typhoon Yagi losses. Underwriting performance is expected to remain robust over the medium term, supported by profitable results in both commercial and retail lines of business. Investment income, consisting mainly of interest and dividend income, is expected to remain a key contributor to the company’s overall earnings.

AM Best assesses PVI Insurance’s business profile as neutral. The company is the largest non-life insurer in Vietnam based on both 2024 and nine months of 2025 direct premiums written. The company has a strong market position in commercial and industrial lines of business, including energy, property, engineering, aviation and marine insurance. Support from HDI V.a.G. has enhanced PVI Insurance’s technical expertise and service offerings, strengthening its position in the regional industrial risks insurance segment. Business expansion in inwards reinsurance was a major contributor to recent growth, although prudent accumulation management remains an area to be monitored.

Ratings are communicated to rated entities prior to publication. Unless stated otherwise, the ratings were not amended subsequent to that communication.

This press release relates to Credit Ratings that have been published on AM Best’s website. For all rating information relating to the release and pertinent disclosures, including details of the office responsible for issuing each of the individual ratings referenced in this release, please see AM Best’s Recent Rating Activity web page. For additional information regarding the use and limitations of Credit Rating opinions, please view Guide to Best’s Credit Ratings. For information on the proper use of Best’s Credit Ratings, Best’s Performance Assessments, Best’s Preliminary Credit Assessments and AM Best press releases, please view Guide to Proper Use of Best’s Ratings & Assessments.

AM Best is a global credit rating agency, news publisher and data analytics provider specialising in the insurance industry. Headquartered in the United States, the company does business in over 100 countries with regional offices in London, Amsterdam, Dubai, Hong Kong, Singapore and Mexico City. For more information, visit www.ambest.com.

Lower premium benefits are prized by employees in today’s economy, but thousands of dollars in unexpected out-of-pocket costs haunt many later

ST. PAUL, Minn.–(BUSINESS WIRE)–

As rising costs continue to outpace wages, many Americans are cutting costs by prioritizing lower premium insurance benefits offered by their employers during open enrollment — often at the expense of long-term financial protection.

The research identifies a growing “affordability trap” — a pattern in which employees choose high-deductible health plans (HDHPs), skip supplemental coverage or reduce voluntary benefits to save on payroll deductions. While these decisions lower immediate monthly costs and produce bigger paychecks, they can result in thousands of dollars in unexpected out-of-pocket expenses later.

“When budgets are tight and enrollment decisions feel overwhelming, employees default to the one number they can control — the premium,” said Adam Taylor, vice president for Employee Benefits Solutions at Securian Financial. “But what looks cheaper today can become far more expensive tomorrow.”

The hidden financial exposure behind “cheaper” plans

Securian Financial’s study found cost dominates benefits enrollment decisions, with nearly two-thirds of employees, especially older generation employees, saying it’s their top workplace benefits priority during open enrollment. Most employees say they choose lower-premium plans with higher deductibles or stick with bare-minimum coverages because it’s all they can afford.

For many employees, the out-of-pockets costs these “cheaper” plans come with can end up hurting them financially and beyond. In the past 12 months:

22% of survey respondents received a surprise medical bill that was higher than expected

20% used savings or emergency funds to pay medical bills

18% experienced significant financial stress due to medical bills

17% went into debt for medical expenses

13% delayed or avoided medical care due to cost concerns

3% filed for bankruptcy or considered it due to medical debt

“The math employees are doing is simple: ‘What comes out of my paycheck?’” said Taylor. “The math they’re not seeing is what happens if they’re hospitalized, need surgery or face a serious diagnosis. That’s where the affordability trap snaps shut.”

Recommendations for employers

The study urges employers to move beyond premium comparisons and make total exposure visible:

Show real-dollar scenarios: Illustrate premium + deductible + out-of-pocket maximum in routine and high-cost years.

Bundle guidance at decision points: If employees select HDHPs, be sure to show them supplemental insurance protections like accident, critical illness and hospital indemnity insurance that can help offset likely exposure. Only 30% of employees surveyed said they were enrolled in supplemental coverage, but 67% who are said they find it helpful.

Invest in scenario-based benefit decision-support tools: 70% of employees said in the study they use these AI-based tools when available.

Design for time-constrained decisions: Lead with the most consequential trade-offs, as the study found one in five employees (20%) feel pressured to decide quickly during open enrollment.

Communicate trade-offs transparently: Explain what has changed since last year, why and what employees should consider next.

“The affordability trap isn’t about employees making bad decisions,” said Emma Thomas, director of marketing at Securian Financial, who leads the company’s annual workplace benefits research. “It’s about employees making rational decisions with incomplete information—and paying for it later. Employers can’t eliminate the trade-offs, but they can make those trade-offs visible.”

Study methodology

Securian Financial’s fourth annual workplace benefits study included a quantitative online survey of 1,000 employees at companies with 1,000+ employees, fielded November 18 to December 1, 2025, and qualitative virtual interviews with eight HR decision-makers at companies with 1,000+ employees, fielded November 10-24, 2025.

ABOUT SECURIAN FINANCIAL

To be confident in your financial future, you need to trust the strength and commitment of the companies you choose to work with. For more than 145 years, the Securian Financial family of companies has been developing innovative insurance and retirement solutions to meet the evolving needs of individuals, families and businesses. Offered through partnerships with employers, financial professionals and affinity groups, our products help bring peace of mind to more than 23 million customers throughout the United States and Canada. We are trusted by our partners and customers to fulfill our purpose of building secure tomorrows. For more information about Securian Financial, visit securian.com or follow us on Facebook, Instagram or LinkedIn.

Securian Financial is the marketing name for Securian Financial Group, Inc., and its subsidiaries. Insurance products are issued by its subsidiary insurance companies, including Minnesota Life Insurance Company and Securian Life Insurance Company, a New York authorized insurer.

Zocks helps turn first meetings into complete case packets, eliminating operational bottlenecks and accelerating time to issue

SAN FRANCISCO–(BUSINESS WIRE)– Zocks, the privacy-first AI assistant for financial advisors, today announced it is bringing its AI-automated operational and document intelligence capabilities to the life insurance market. Zocks is already in use exclusively at two of the three largest U.S. life insurance carriers.

Zocks captures and creates accurate notes on household, financial, and life details during a discovery meeting, then automatically completes paperwork including carrier applications, fact finders, and client intake forms. Documentation in any format, including PDFs, scans, and photos, is also automatically processed in less than 60 seconds and synced to applications and forms.

Zocks also automatically syncs relevant client information from meetings and documents to customer relationship management (CRM) systems, illustration, and other planning tools, further reducing time-intensive data entry.

Additionally, Zocks extracts client details required for needs analysis, suitability, case design, and other essential administrative work that, when incomplete or done improperly, results in back-and-forth underwriting delays and long “Not In Good Order” (NIGO) cycles.

The result is faster, cleaner applications, quicker follow-ups for a better client experience, and ultimately more policies issued per month.

Beyond application and underwriting support, Zocks automates meeting preparation, follow-up emails, and client communications to keep momentum between meetings. It identifies important details like missing items, exam scheduling, beneficiary confirmations, delivery requirements, and payment setup, so advisors can provide faster, more personalized service.

“Zocks speeds up our workflow after calls, letting us send emails and meeting notes quickly during our short breaks,” said Jack Rogers, Case Manager at Strategic Wealth Group, a Guardian Life agency. “We are in meetings back-to-back all day, so in the past we would wait until the day ended to post case planning notes to the team and send out follow-ups. Now, we can do it in between calls.”

Zocks also addresses one of the insurance sector’s most persistent challenges: recruiting and retaining productive agents. Industry commentators, citing Bureau of Labor Statistics (BLS) age data, estimate that roughly 50% of today’s insurance workforce could retire over the next decade.

Zocks’ performance tracking helps firms identify what their best producers do well and replicate it across the organization, including the ability to rate meetings across 18 configurable dimensions and benchmarked against industry standards. Leaders now have data-driven insights to coach producers and close the gap between top performers and the rest of the team.

“Life insurance professionals face a unique combination of high meeting volume, complex documentation requirements, and thin margins for error,” said Mark Gilbert, CEO of Zocks. “The firms that win in this competitive market are using AI to remove friction at every step, from the first meeting to the issued policy to client retention. Zocks gives producers and leaders the capacity and insights to do that at scale.”

Zocks is the AI Assistant for financial services. Its privacy-first platform saves advisors 10+ hours a week by automating administrative tasks like meeting preparation and notes, intake and account opening forms, tailored client emails, document processing, and more. With powerful integrations and enterprise-ready controls, Zocks turns every client conversation into structured, accurate data and insights that strengthen relationships and fuel business growth. Join thousands of advisors and firms, including Carson Group, Osaic, Kestra Financial, and Ameritas, that rely on Zocks; learn more and start a free trial at zocks.io.

When a loved one dies, family members have a number of things they must do. In addition to making funeral arrangements, survivors must take care of the loved one’s estate to the best of their ability. Family members often wonder if their loved one had a life insurance policy.

While the staff at the Department of Insurance can’t help you probate a person’s will, we can help you locate a lost life insurance policy. The service is free and helps locate benefits from life insurance policies or annuity contracts purchased in North Carolina.

You can find the Lost Life Insurance and Annuity Service on the Department of Insurance’s web page at: ncdoi.gov. Scroll down and click on the link that says, “Locate a lost life insurance policy.” After agreeing to the terms and conditions, you will be asked to provide some information about yourself and the deceased.

If you’re having trouble or need assistance, you can call our toll-free number at: (855) 408-1212 to speak to one of our consumer specialists. Call between 8 a.m. and 5 p.m. on weekdays.

The program works. Last year, the tool helped North Carolinians obtain $65.9 million in claims from life insurance policies that had been lost. In 2024, North Carolinians obtained $70.5 million in life insurance benefits. In 2023, the service found $65.9 million in benefits.

People purchase life insurance policies for several reasons. They may want to:

· Allow a surviving spouse to continue having a comfortable standard of living.

· Make retirement more comfortable.

· Provide for a child’s education.

· Pay for funeral expenses. · Pay for medical bills. · Pay off a mortgage so surviving family members don’t have to worry about having a roof over their head.

· Pay off other outstanding debts.

Whatever the reason for taking out a life insurance policy, beneficiaries expect to be able to receive those benefits when a loved one dies.

The life insurance policy may have been taken out years or decades ago. Families may have moved over the years. The policy may have been misplaced or accidentally thrown away. Searching through a safe, desk drawers or filing cabinets may yield no results.

Fortunately, this tool is available to help families during difficult times. Losing a loved one is difficult enough.

You may want to keep our toll-free number handy in case you have other questions regarding insurance.

N.C. Department of Insurance Commissioner Mike Causey.

Strong earnings, surplus growth and the largest dividend in company history reflect successful execution of company’s long-term strategy

NEW YORK–(BUSINESS WIRE)–

New York Life, America’s largest¹ mutual life insurer, today announced record financial results for 2025, reflecting the strength of its mutual structure, diversified business model, and disciplined capital management.

The company delivered $3.6 billion in earnings,2 a four percent increase over the prior year, and grew surplus to $34.7 billion,3 up from $33.3 billion in 2024. Supported by this strong performance, New York Life declared a $2.8 billion dividend4 to eligible participating policy owners, the largest in company history, continuing its 172-year track record of paying dividends.

“In 2025, we grew earnings, strengthened our capital position, and declared the largest dividend in our history,” said Craig DeSanto, Chair, President & CEO of New York Life. “As a mutual company, we operate for our policy owners — not shareholders — which allows us to take a long-term view, share our success with those who rely on us, and focus on what matters most: helping our clients build financial security and peace of mind.”

Sustained Financial Strength

New York Life’s surplus growth continues to underpin its superior financial strength. In 2025, the company again earned the highest possible financial strength ratings currently awarded to U.S. life insurers from all four major rating agencies.5

The company’s consistent capital growth, diversified earnings, and prudent risk management are designed to ensure it can meet its obligations across economic cycles.

Diversified Business Model

New York Life’s performance was supported by its broad-based growth across its diversified businesses.

In 2025:

Insurance sales increased 14 percent6

Annuity sales increased 40 percent7

Mutual fund sales increased 7 percent8

Collectively, New York Life policy owners now hold nearly $1.3 trillion in individual life insurance,9 reflecting the company’s long-standing focus on delivering protection-first financial security.

This diversified growth strengthens New York Life’s capital position and supports its ability to deliver long-term value to participating policy owners.

Investing to Deliver Enhanced Client and Advisor Experiences

“We continue to invest to make it easier to do business with New York Life,” said DeSanto. “That includes expanding digital capabilities, leveraging artificial intelligence, and strengthening the technology that supports our operations — all with a focus on enhancing service, security, and long-term value.”

Financial Performance Highlights for the Year Ended Dec. 31, 2025

$3.6 billion in operating earnings2

$34.7 billion in surplus (including the asset valuation reserve)3

$2.8 billion dividend declared for payment in 20264

$18.1 billion in policy owner benefits and dividends10

$892 billion in assets under management11

Nearly $1.3 trillion in individual life insurance protection in force9

ABOUT NEW YORK LIFE

New York Life Insurance Company (www.newyorklife.com), a Fortune 100 company founded in 1845, is the largest1 mutual life insurance company in the United States and one of the largest life insurers in the world. Headquartered in New York City, New York Life’s family of companies offers life insurance, disability income insurance, retirement income, investments and long-term care insurance. New York Life has the highest financial strength ratings currently awarded to any U.S. life insurer from all four of the major credit rating agencies.5

“New York Life” or “the company,” as used throughout the press release, can refer either separately to the parent company, New York Life Insurance Company (NYLIC), or one of its subsidiaries, or collectively to all New York Life companies, which include NYLIC and its subsidiaries and affiliates, including New York Life Insurance and Annuity Corporation (NYLIAC), NYLIFE Insurance Company of Arizona (NYLAZ), Life Insurance Company of North America (LINA), and New York Life Group Insurance Company of NY (NYLGICNY). NYLAZ and LINA are not authorized in New York and do not conduct insurance business in New York. LINA and NYLGICNY are referred to as the New York Life Group Benefit Solutions business. Any discussion of ratings and safety throughout the press release applies only to the financial strength of New York Life, and not to the performance of any investment products issued by the company. Such products’ performances will fluctuate with market conditions.

1Based on revenue as reported by “Fortune 500 ranked within Industries, Insurance: Life, Health (Mutual),” Fortune magazine, 6/2/2025. For methodology, see https://fortune.com/company/new-york-life-insurance/.

2Operating earnings is the measure used for management purposes to track the company’s results from ongoing operations and the underlying profitability of the business. This chart is based on Statutory Accounting principles on insurance operations with certain adjustments we believe are more appropriate as a measurement approach.

The New York State Department of Financial Services recognizes only unadjusted statutory accounting practices for determining and reporting the financial condition and results of operations of an insurance company, for determining its solvency under the New York Insurance Law, and for determining whether its financial condition warrants the payment of a dividend to its policy owners. Policy owners can view a detailed reconciliation of our management performance measure by visiting our website, www.newyorklife.com, beginning in mid-March.

3Total surplus, which includes the AVR, is one of the key indicators of the company’s long-term financial strength and stability and is presented on a consolidated basis of the company. NYLIC’s statutory surplus was $27.6 billion and $26.4 billion at December 31, 2025 and 2024, respectively. Included in NYLIC’s statutory surplus is NYLIAC’s statutory surplus totaling $8.6 billion and $8.4 billion at December 31, 2025 and 2024, respectively, and LINA’s statutory surplus of $2.3 billion and $2.2 billion at December 31, 2025 and 2024, respectively. AVR for NYLIC was $4.7 billion and $4.6 billion at December 31, 2025 and 2024, respectively. AVR for NYLIAC was $2.3 billion and $2.1 billion at December 31, 2025 and 2024, respectively. AVR for LINA was $0.2 billion and $0.2 billion at December 31, 2025 and 2024, respectively.

4Dividends are not guaranteed. New York Life Insurance Company is a mutual company that issues participating products that are eligible for dividends, but is also the parent of subsidiaries which issue non-participating products. The participating products are invested in separate and distinct portfolios and have their own dividend scales.

5Individual independent rating agency commentary as of 10/28/2025: A.M. Best (A++), Fitch (AAA), Moody’s Investors Service (Aa1), Standard & Poor’s (AA+).

6Insurance sales represent annualized first-year premiums on participating issued whole life insurance, term life insurance, universal life insurance, long-term care insurance, disability insurance, and other health insurance products. A sale is generally counted when the initial premium is paid and the policy is issued. Adjustments are made to normalize nonrecurring premiums to align with our annualized recurring premium methodology for insurance sales. Some examples are: single-premium individual and Corporate Owned Life Insurance products sold through our agents and third party distribution channels, which are counted in this metric at 10 percent of their premium. Sales are generated from both domestic and Mexican operations.

7Total annuity sales represent premiums on our deferred annuities (both fixed and variable) and on our guaranteed income annuities. Sales are generally recognized when premiums are received. Annuities are primarily issued by NYLIAC.

8Mutual fund sales represent total cash deposited primarily to new and existing accounts of the New York Life Investments (NYLI) Funds, New York Life’s proprietary mutual funds. NYLI Funds are managed by New York Life Investment Management LLC and distributed through NYLIFE Distributors LLC, an indirect wholly owned subsidiary of NYLIC.

9Individual life insurance in force is the total face amount of individual life insurance contracts (term, whole, and universal life) outstanding for NYLIC and its domestic insurance subsidiaries at a given time. The company’s individual life insurance in force totaled $1,264.5 billion and $1,227.3 billion at December 31, 2025 and 2024, respectively (including $193.7 billion and $183.6 billion for NYLIAC at December 31, 2025 and 2024, respectively).

10Policy owner benefits primarily include death claims paid to beneficiaries and annuity payments. Dividends are payments made to eligible policy owners from divisible surplus. Divisible surplus is the portion of the company’s total surplus that is available, following each year’s operations, for distribution in the form of dividends. Dividends are not guaranteed. Each year the board of directors votes on the amount and allocation of the divisible surplus. Policy owner benefits and dividends reflect the consolidated results of NYLIC and its domestic insurance subsidiaries. Intercompany transactions have been eliminated in consolidation. NYLIC’s policy owner benefits and dividends were $9.5 billion and $9.1 billion for the years ended December 31, 2025 and 2024, respectively. NYLIAC’s policy owner benefits were $6.3 billion and $6.3 billion for the years ended December 31, 2025 and 2024, respectively. LINA’s policy owner benefits were $1.9 billion and $1.9 billion for the years ended December 31, 2025 and 2024, respectively. Benefits have been adjusted to exclude implications of a strategic reinsurance transaction.

11Assets under management consist of cash and invested assets and separate account assets of the company’s domestic and international insurance operations, and assets the company manages for third-party investors, including mutual funds, separately managed accounts, retirement plans, and assets under administration.

The company’s general account investment portfolio totaled $371.6 billion at December 31, 2025 (including $140.3 billion invested assets for NYLIAC and $8.6 billion invested assets for LINA). At December 31, 2025, total assets equaled $463.5 billion (including $223.5 billion total assets for NYLIAC and $9.5 billion total assets for LINA). Total liabilities, excluding the Asset Valuation Reserve (AVR), equaled $428.8 billion (including $212.6 billion total liabilities for NYLIAC and $7.0 billion total liabilities for LINA). See Note 3 for total surplus.

Where applicable, prior period numbers have been restated to conform to the current-year definition. In addition, non-U.S.-denominated results are generally valued using applicable year-end exchange rates.

A copy of our statutory financial statements and reconciliation to our performance measure are also available by writing to the Secretary of New York Life Insurance Company, 51 Madison Avenue, New York, NY 10010.

My dad may very well live another 20 years or more, but last week the three of us — my dad, my sister and I — spent a day doing something most people avoid for as long as possible: we visited the cemetery and made his funeral arrangements. We picked out his future burial plot. We designed the gravestone that will one day bear his name beside my mom’s. And later, over lunch, we met with the cremation company so he could prepay for his services and document his final wishes.

On paper, it was a day about death.

In reality, it was a day about love.

Lori Seaton

It was emotional, absolutely. Vulnerable, yes. But underneath the heaviness was an unmistakable truth: My dad was giving us a gift. A gift of peace, clarity, and preparation. A gift he knew we would need someday — and one he was brave enough to give while he was still here.

The plot with the sunny ‘neighborhood’

My mom passed a couple of years ago after an unexpected ALS diagnosis. She was healthy, vibrant – the last person anyone thought would leave us first. Her death altered our understanding of preparation in a way nothing else could have. It also shaped how we approached this day — our unusual family outing to choose a future resting place for our parents (my mom’s urn currently rests on dad’s mantle).

Despite the emotional weight, we found ourselves laughing in the way only families who love each other deeply can. My mom was incredibly social and full of life, so as we walked through the cemetery looking at potential plots, we joked about wanting to choose one in a “good neighborhood”—you know, a fun group of couples for Mom and Dad to hang out with for eternity.

We wanted sunlight too. Mom loved the sun. She loved tanning. So of course, her spot needed sunshine. It was ridiculous and tender at the same time, us trying to make sense of a moment that was both profoundly sad and strangely intimate.

Only a family that knows how to love through loss can laugh while standing in a cemetery.

The prayer that captured everything

Eventually, we found a section of the cemetery called “Peace.” It felt right immediately, but it wasn’t until we noticed the statue nearby that the meaning of the day really landed.

On the statue was the prayer of St. Francis:

Lord, make me an instrument of your peace.

Where there is hatred, let me sow love.

Where there is injury, pardon; where there is doubt, faith;

Where there is despair, hope;

Where there is darkness, light;

And where there is sadness, joy.

I read it once, then again. Each line hit me deeper – because that’s exactly what my dad was doing for us.

He was sowing love through preparation.

He was giving us faith that his wishes would be honored.

He was offering hope that someday, when the time comes, the logistical burden won’t overshadow our grief.

He was shining light on something most families only face in the dark.

And he was giving us joy, odd as that sounds—joy in knowing we would not carry the confusion or stress that so often accompanies loss.

Standing there in the Peace section, I realized:

This wasn’t just a plot. It was his final act of protection.

The wallet card we never knew about

After choosing the plot, we drove back to the cemetery office to design the gravestone. That part felt especially surreal — selecting fonts and layouts for something that won’t be used for years, maybe decades. But my dad approached it with calm practicality, the same way he does everything.

And then something unexpected happened. As we were finalizing the design, my dad suddenly remembered a small, engraved metal card my mom had once given him. He pulled out his wallet, and there it was — worn from years of being carried, but still legible.

He read the final line: “My best friend, my soulmate, my everything.”

My sister and I had never seen this card. We never would have included this line on the gravestone — could never have known to. But in that moment, my dad gave us a piece of their love story. A piece that will now live in stone. A piece of them, and we added it immediately.

And even he seemed relieved — maybe proud — to know that this sentiment, one my mom gave him in life, will carry forward into memory.

This is the kind of detail planning now allows.

This is the kind of meaning families miss when decisions are made in grief.

Lunch and the second layer of his gift

After leaving the cemetery, we had lunch with the people from the cremation company. Here is another step most families avoid thinking about until they are forced to: my dad prepaid for the company’s services — taking another weight off our future shoulders. He’ll complete a document outlining his final wishes, ensuring we’ll never have to guess. We won’t have to wonder what he wanted. We won’t second-guess ourselves. We won’t worry whether we’re doing something wrong.

He is removing the load before we ever have to carry it.

The red file folder

What strikes me most is that this day wasn’t a one-time act. It’s part of a larger pattern of love and preparation he has carried out since my mom died.

My dad is a planner, but he is also incredibly loving. Those two qualities together have resulted in something remarkable: a bright red file folder containing everything his daughters might need someday, including a list of all his financial accounts, points of contact, power of attorney documents, his will and instructions.

He walked us through it — where it’s stored, what’s inside, what to do. It was equally heartbreaking and comforting. That folder is his way of continuing to parent us, even when he won’t physically be here to do it.

And let me tell you: few things bring more relief than knowing your future self will have answers during a time when you desperately need them.

Losing mom changed everything

When my mom was diagnosed with ALS, none of us saw it coming. She had always been healthy, the one we all assumed would outlive my dad by years, maybe decades. Life doesn’t follow our assumptions. It throws curveballs we never saw coming, and it rarely asks permission first. Her illness and death taught us a painful truth: We do not get to choose the timing. But we can choose the preparation.

My dad understood that, and he chose to act.

What I felt most strongly: relief

I expected sadness and heaviness. What surprised me was the overwhelming sense of relief.

Most families make these decisions while drowning in grief. Emotions are raw, time is short, and everyone is terrified of making the wrong choice.

But because of my dad’s gift, we won’t have to do that. We will not face a dozen impossible decisions on the worst day of our lives. We will not wonder what he would have wanted.

We will not spend our early grieving days in conference rooms, choosing things we wish we weren’t choosing.

We will get to grieve. Fully, honestly and without chaos.

That is the gift.

Why I’m sharing this: A call to action

I’m writing this because I want others to feel what we felt that day — not the sadness, but the clarity and empowerment. The quiet sense of peace that comes from knowing the future will not be a mystery.

These conversations are difficult, and these decisions are emotional. No one wants to imagine the day their loved ones will need this information. But it is worth it. I can tell you, it is incredibly, profoundly worth it. The gift of preparation is one of the greatest acts of love you can offer your family.

Have the conversations sooner.

Make the decisions sooner.

Fill the folder.

Choose the plot.

Write the wishes.

Do it while you can bring humor, memory and intention into the process. Don’t wait for a crisis to make the choices for you.

A day of peace, a legacy of love

As we walked back through the “Peace” section of the cemetery that day, the prayer of St. Francis stayed with me. Each line mirrored what my dad had just given us — love, faith, hope, light and even joy. His preparations were not about dying. They were about living —living in a way that protects his daughters long after he’s gone. And that, I’ve learned, is what love looks like at its most unselfish. A gift of peace when your loved ones will need it most. And my dad gave us that gift long before we’ll ever need to use it.

Fort Worth, Texas — National Farm Life Insurance Company (NFLIC) announced today that its Board of Directors has elected Dr. Kyle W. McGregor, Chairman, President and Chief Executive Officer, to serve as Chairman of the Board, effective immediately following the company’s Annual Stockholders Meeting.

Dr. McGregor has served as a member of the company’s Board of Directors since 2009 and succeeds J.D. “Chip” Davis, who is stepping away from the role after a distinguished tenure of leadership with the company.

Dr. McGregor previously served as President and Chief Executive Officer of NFLIC. He joined the company as an employee in 2020 and has played a key role in guiding the company’s strategic growth, strengthening its financial position, and expanding its commitment to serving policyholders and agents across Texas. Since 2021, the company has experienced measurable growth under his leadership, including a 5% increase in issued premium, an 11% increase in first-year collected premium, a 4% increase in net admitted assets, and a 19% increase in capital and surplus. Twice during this period, the company has set new historical production records. Prior to joining the company as an employee, Dr. McGregor was elected to the Board of Directors in 2009 and has contributed to the company’s governance and long-term strategic direction for more than a decade.

As Chairman, President and Chief Executive Officer, Dr. McGregor will continue to lead the company while working closely with the Board of Directors to advance NFLIC’s long-term mission and strategy.

“I am honored by the Board’s trust and grateful for the opportunity to serve as Chairman,” said Dr. McGregor. “I appreciate the confidence and support of our entire Board of Directors and the leadership each of them brings to National Farm Life. I am especially grateful to Chip Davis for his service as Chairman, and National Farm Life’s officers for their expertise and many years of dedication to the company. I look forward to continuing to work with the Board as we guide National Farm Life into its next chapter.”

About National Farm Life Insurance Company

Celebrating its 80th Anniversary, NFLIC was founded in 1946 in the Historic Fort Worth Stockyards. The company offers products through more than 1,300 independent agents and is dedicated to providing life insurance solutions designed to help families and individuals achieve financial security and long-term peace of mind. NFLIC remains committed to strong financial performance, policyholder value, and trusted service through its network of independent agents

WOBURN, Mass.–(BUSINESS WIRE)–

SBLI today announced that its popular EasyTrak Digital Term product just got even better. In addition to the product’s existing built-in benefits, EasyTrak now automatically includes a Chronic Illness Rider, at no extra premium cost.

Designed with both affordability and convenience in mind, EasyTrak continues to deliver simple, streamlined protection. The Chronic Illness Rider allows eligible policyholders who meet rider criteria as certified by a physician to accelerate up to 50% of their death benefit, to a maximum of $250,000. The benefit is automatically included in the policy, making it easier than ever for clients to be financially empowered when they need it most.

“EasyTrak has always been about removing barriers and making life insurance simple,” said Wade Seward, SBLI Chief Distribution Officer. “With the addition of the Chronic Illness Rider at no additional premium cost, we’ve enhanced the product’s value while maintaining the speed and ease that agents and clients require.”

Affordable Protection — Built for Today’s Needs

EasyTrak is designed to help agents get coverage in place quickly and efficiently, offering:

Instant decisions on all applications;

Ability to instantly edit coverage; and

Quote-to-issue in just nine minutes.

Terminal illness benefits were already included, and with the addition of the Chronic Illness Rider, EasyTrak delivers expanded living benefits – without added premium or time to issue.

“With its fully digital experience, EasyTrak empowers agents to move at the speed of their clients’ lives,” Seward added. “By combining affordability, speed, and built-in living benefits, EasyTrak continues to raise the bar for modern term life insurance.” To learn more about EasyTrak, please visit SBLI Easytrak Digital Term – SBLI Partners.

About SBLI

For more than 115 years, SBLI (The Savings Bank Mutual Life Insurance Company of Massachusetts) has offered simple, dependable life insurance solutions to families across the United States. With a focus on clarity, personal support and long-term trust, SBLI provides term and whole life products that help people protect what matters most. For more information, visit www.sbli.com.

Indexed universal life insurance hit a milestone in 2024: $3.8 billion in new premiums, capturing 24% of the total U.S. life insurance market. Yet IUL remains one of the most misunderstood and often misrepresented products in our industry.

Ian McDowell

IUL is a type of long-term whole life insurance policy that can be maintained via flexible premium payments, provides a death benefit to beneficiaries and has the opportunity for cash value accumulation. The cash value may earn credited interest based on the performance of an external market-linked index, subject to caps, rates and spreads.

For agents, ethical communication is the difference between sustainable success and short-term wins that damage your reputation. The agents who thrive don’t oversell benefits. They explain mechanics with transparency that builds professional trust.

Why transparency creates loyal clients

Kaiser Family Foundation (KFF) research reveals that half of insured adults struggle to understand their coverage. Specifically, 36% don’t know what their insurance covers. Yet clients working with transparent financial professionals report significantly higher satisfaction and loyalty.

The regulatory environment reinforces this reality. AG49-B regulations, effective since May 2023, eliminated experience refunds, multipliers and bonuses from illustrations — requiring you to show only actual index credits.

Try this opening approach: “I want to educate you on how IUL works, including its limitations, before we discuss whether it makes sense for you. I’d rather you make an informed decision, even if that means this isn’t the right fit, than sell you something you don’t fully understand.”

This transparency increases close rates. Clients trust that you’re putting their interests first. One of the best ways to help them visualize transparency is the client reality test. I always present two scenarios:

The illustrated projection

The alternate scale with conservative assumptions

Then ask:“If reality lands closer to the conservative scenario, does this still meet your objectives?”

If the answer is no, explore other options. About 30% of prospects decline at this point—and that’s exactly what should happen. IUL isn’t appropriate for everyone. Walking away from a commission preserves your reputation far more than forcing a bad fit.

Understanding IUL tax mechanics

Clarity on tax mechanics is what either builds or destroys credibility. Walk every client through the distinction between policy loans and withdrawals using real numbers from their specific illustration.

The policy loan reality check:

“When we discuss ‘tax-free income,’ we’re talking about policy loans. You borrow from the insurance company at [current rate], while your full cash value continues to earn index credits. These loans remain generally tax-free if the policy remains in force, allowing access to up to 90% of the policy’s cash value without immediate tax liability.”

“If you’re earning 8% and paying 5% on the loan, you’re earning a 3% arbitrage. But here’s what most agents won’t tell you: If performance lags for years and loan interest compounds, the policy can lapse and trigger a massive tax bill on phantom income you never actually received. That’s why we monitor this quarterly and adjust loan amounts based on actual performance.”

The withdrawal distinction:

“Withdrawals operate differently. They’re tax-free only up to your cost basis, which is the total premiums you’ve paid. Anything above that gets taxed as ordinary income and permanently reduces your death benefit. We use loans strategically when you need access and only consider withdrawals when you’re certain you won’t need that coverage later.”

Maximum-funded IUL policies use the lowest legally allowable death benefit and fund to IRS non-modified endowment contract limits over 4-7 years. This helps minimize annual insurance costs to 0.8%-1.5% of the cash value.

Essential discovery questions:

Walk me through your current retirement savings. Have you maxed out your 401(k) and individual retirement account contributions?

How do you feel about market volatility? Tell me about a time when a downturn impacted your decisions.

What’s your timeline? When do you need to access this money?

Would you commit to quarterly reviews, even if that means adjusting premiums when performance lags?

How does your retirement savings plan react to your death? Are loved ones covered? Do you have a succession plan?

Remember that an IUL may not be the answer for a client’s specific needs or goals. IUL typically doesn’t work for clients who:

Need short-term coverage (term life costs less)

Want simplicity (whole life is straightforward)

Can’t commit to quarterly reviews

Are within 10 years of retirement

Have limited premium budgets

Building your practice on ethical IUL education

Match the product to the client, not the client to the product. This principle separates successful agents from those constantly chasing new business. When you master this consultative approach, you create clients who become your best advocates. They refer you to others because they genuinely understand and value what you’ve built for them.

Transparency drives retention. At every quarterly review, they show clients their actual credit rates alongside the original illustrations. When performance lags, have real conversations about their options: increasing premiums, adjusting loan amounts or modifying the death benefit. This honest dialogue builds trust that lasts.

Don’t overemphasize the upside of IULs. Start educating clients on realistic expectations, be transparent about them, and outline appropriate risk profiles and proper policy structure. Choose to be an educator and enhance your success.

The clients who truly understand their strategy stay. The ones who don’t, leave. Choose which practice you want to build.

Despite several high-profile lawsuits and continued market turbulence, indexed life insurance remains the preferred product for consumers.

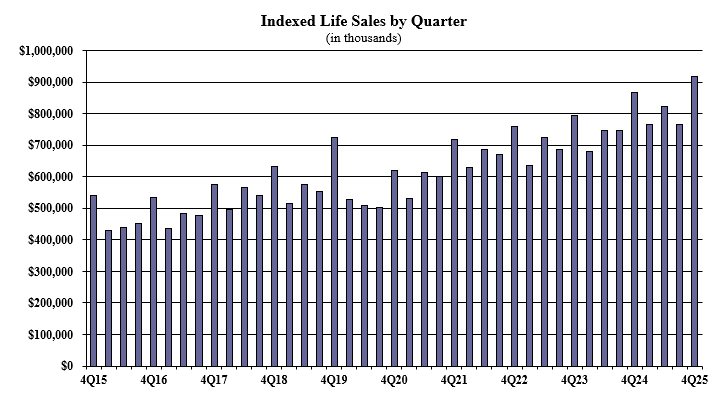

Indexed life sales for the fourth quarter were $918.9 million, up 20% compared with the previous quarter, and up 6.2% compared to the record set in Q4 2025, Wink Inc. reported in its Sales & Market Report. Total 2025 indexed life sales were $3.2 billion.

Indexed life sales set both a quarter and yearly record, Wink found. Transamerica Life’s Financial Foundation IUL II, an indexed universal life product, was the No. 1 selling product for all life sales, for all channels combined, for the third consecutive quarter, Wink said.

“Indexed life sales have been setting records since a lull in 2020,” said Sheryl J. Moore, CEO of both Moore Market Intelligence and Wink Inc. “I am intrigued on how recent litigation will impact sales, going forward.”

IUL sellers are currently facing a wave of legal challenges centered on allegations of misleading marketing and unrealistic performance illustrations. In February, Pacific Life agreed to a $58.3 million settlement to resolve a lawsuit claiming it used deceptive illustrations to sell policies, shortly followed by a private settlement with NASCAR champion Kyle Busch, who alleged losses of over $8.5 million.

Meanwhile, National Life Group is defending a renewed lawsuit in Vermont where plaintiffs label its proprietary indices a “fraudulent sham” for using back-tested data that fails to match real-world 0% returns.

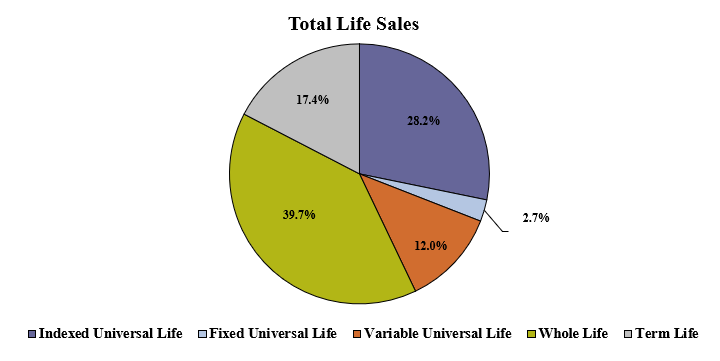

All life insurance sales for the fourth quarter were over $3.2 billion, up 14.9% compared to the previous quarter and up 3.2% compared to the same period last year. Total 2025 sales of all life insurance were $11.7 billion. All life sales include fixed universal life, indexed UL, variable UL, indexed whole life, whole life and term life product sales.

Courtesy of Wink, Inc.

Massachusetts Mutual Life Companies ranked as No. 1 in overall for all life sales, with a market share of 6.8%, Wink reported.

Wink’s full life insurance breakdown for Q4 and the full year, by product category:

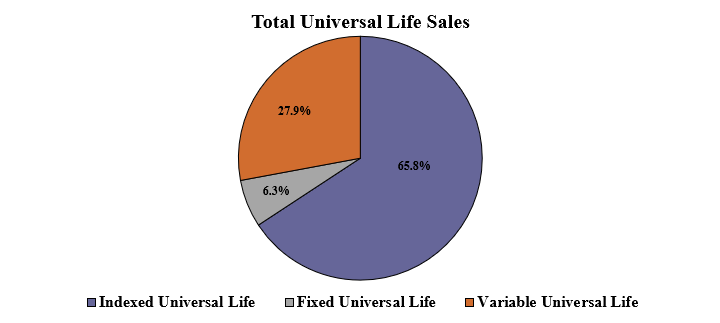

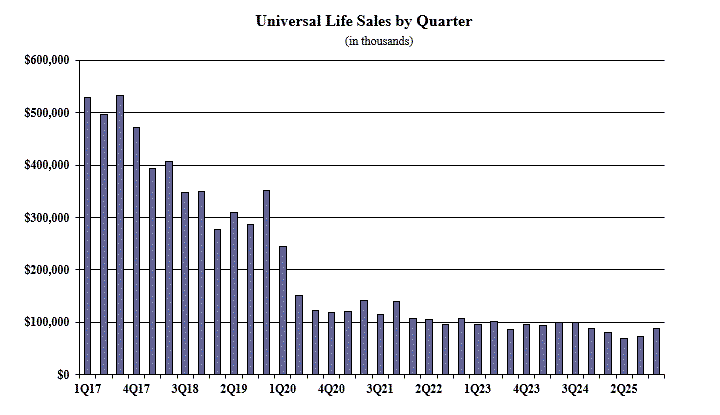

All universal life sales for the fourth quarter were over $1.3 billion, up 20.9% compared to the previous quarter and up 5.2% compared to the same period last year. Total 2025 sales of all universal life products were $4.8 billion. All universal life sales include fixed UL, indexed UL, and variable UL product sales.

Noteworthy highlights for all universal life sales in the fourth quarter included Pacific Life Companies ranking as No. 1 in overall sales for all universal life sales, with a market share of 12.5%.

Courtesy of Wink, Inc.

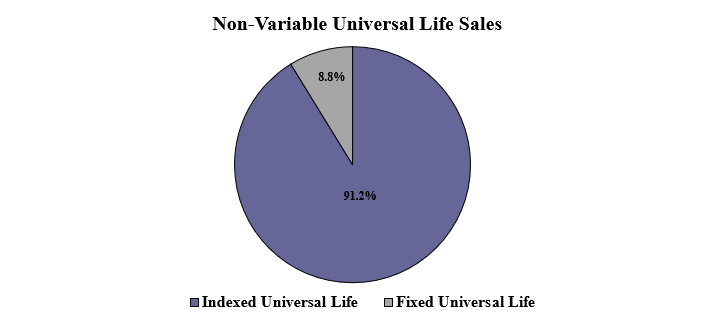

Non-variable universal life sales for the fourth quarter were $1 billion, up 20.3% when compared to the previous quarter and up 5.6% compared to the same period last year. Total 2025 non-variable UL sales were $3.5 billion. Non-variable universal life sales include both fixed UL and indexed UL product sales.

Noteworthy highlights for total non-variable universal life sales in the fourth quarter included National Life Group retaining the No. 1 overall sales ranking for non-variable universal life sales, with a market share of 14%.

Courtesy of Wink, Inc.

Fixed universal life sales for the fourth quarter were $88 million, up 21.2% compared to the previous quarter and down 0.6% compared to the same period last year. Total 2025 fixed UL sales were $309.8 million.

Items of interest in the fixed UL market included Nationwide retaining its No. 1 ranking in fixed universal life sales, with a 18.4% market share; Prudential, Pacific Life Companies, John Hancock, and Thrivent Financial completed the top five, respectively.

Pacific Life’s PL Promise GUL was the No. 1 selling fixed universal life insurance product, for all channels combined, for the quarter. The top primary pricing objective, with a no-lapse guarantee, captured 34.1% of sales. The average fixed UL target premium for the quarter was $8,765, an increase of more than 19% from the prior quarter.

Courtesy of Wink, Inc.

Indexed life sales for the fourth quarter were $918.9 million, while total 2025 indexed life sales were $3.2 billion. The record-setting year for indexed life sales topped the prior 2024 record by 8.1%. Indexed life sales include both indexed UL and indexed whole life.

Items of interest in the indexed life market included National Life Group retaining its No. 1 ranking in indexed life sales, with a 15.3% market share; Pacific Life Companies, Transamerica, John Hancock and Nationwide rounded out the top five, respectively.

Transamerica Life’s Financial Foundation IUL II was the No. 1 selling indexed life insurance product, for all channels combined, for the fifth consecutive quarter. The top primary pricing objective for sales in the quarter was cash accumulation, capturing 73.8% of sales. The average indexed life target premium for the quarter was $13,293, an increase of nearly 7% from the prior quarter.

Courtesy of Wink, Inc.

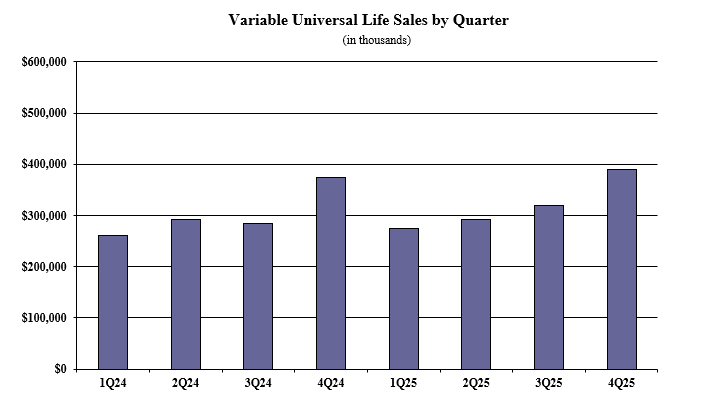

Variable universal life sales for the fourth quarter were $391 million, up 22.4% compared with the previous quarter and up 4.3% compared to the same period last year. Since Wink began tracking sales of these products in 2024, it was a record-setting quarter for variable universal life sales, topping the prior 4th quarter, 2024 record by 4.3%.

Total 2025 variable UL sales were $1.2 billion. It was also a record-setting year for variable universal life sales, topping the prior 2024 record by 5.3%.

Items of interest in the variable universal life market included Prudential retaining the No. 1 ranking in variable universal life sales, with a 28.1% market share; John Hancock, Pacific Life Companies, Nationwide and Lincoln National Life completed the top five, respectively.

Pruco Life’s Prudential FlexGuard Life IVUL was the No. 1 selling variable universal life product, for all channels combined for the quarter. The top primary pricing objective for sales this quarter was cash accumulation, capturing 76.6% of sales. The average variable universal life target premium for the quarter was $25,659, an increase of nearly 14% from the prior quarter.

“No doubt that variable UL sales will be down in 2026,” explained Moore. “Volatility in the markets usually translates to declining sales of both variable annuities and variable UL.”

Courtesy of Wink, Inc.

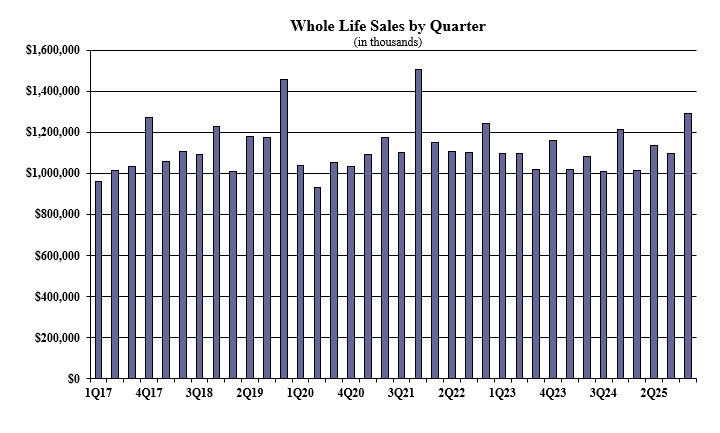

Whole life fourth quarter sales were over $1.2 billion, up 17.4% compared with the previous quarter, and up 6.1% compared to the same period last year. Total 2025 whole life sales were $4.5 billion. Items of interest in the whole life market included the top primary pricing objective of final expense, capturing 70.2% of sales. The average premium per whole life policy for the quarter was $4,786, an increase of more than 20% from the prior quarter.

Courtesy of Wink, Inc.

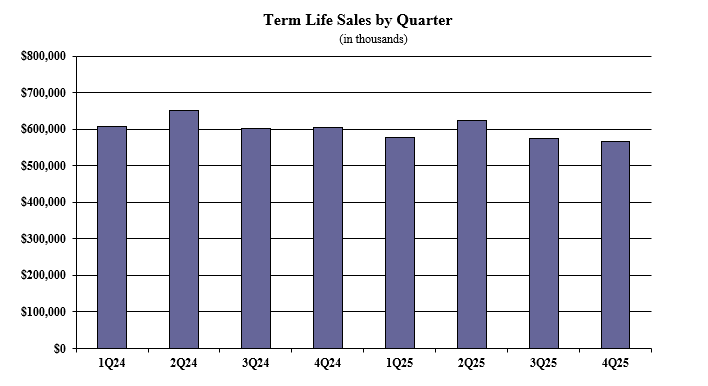

Term life fourth quarter sales were $565.2 million, down 1.6% compared with the previous quarter and down 6.4% compared to the same period last year. Total 2025 term life sales were $2.3 billion.

Items of interest in the term life market include Pacific Life Companies ranking as No. 1 in term life sales, with a 5.5% market share. Prudential, Corebridge Financial, Protective Life Companies and National Life Group completed the top five, respectively.

Pacific Life’s Promise Term 20 was the No. 1 selling term life insurance product, for all channels combined, for the quarter. The average annual term life premium per policy reported for the quarter was $2,678, an increase of more than 20% from the previous quarter.

Courtesy of Wink, Inc.

Wink now reports sales on all annuity lines of business, as well as all life insurance product lines.