Pradip Patiath, Securian Financial board member and McKinsey & Company senior partner

Patiath is a senior partner at McKinsey & Company and a senior global leader in the firm’s Financial Services and Digital practices. For nearly three decades, he has advised organizations across the financial services industry on strategy, growth, AI, digital transformation and large-scale performance improvement.

“Pradip brings deep expertise at the intersection of financial services, technology and innovation,” said Chris Hilger, Securian Financial’s chairman, president and CEO. “His extensive experience advising leading financial services companies on growth, AI and digital transformation will provide valuable insight as we continue advancing our strategy and delivering long-term value for our customers and partners.”

Prior to joining McKinsey, Patiath served as president at CCC Information Services (now CCC Intelligent Solutions), an enterprise software company serving the insurance and financial technology sector. Earlier in his career, he held leadership roles at Honeywell and Schlumberger (now SLB), and he was awarded a U.S. patent in the field of real-time digital transaction systems.

Patiath is active in several civic, educational and nonprofit organizations. He currently serves on the Smithsonian Institution’s national board, the board of the Frost Museum of Science in Miami, the global advisory board of Northwestern University’s Kellogg School of Management and the investment advisory board of the Indian Institute of Technology. He also serves as vice chair of the Chicago Humanities board and previously served as board chair of the Adler Planetarium of Chicago. In the private sector, he recently joined the board of directors of Verisk, a global data analytics and technology provider to the insurance industry.

Patiath holds an MBA with distinction from Northwestern University’s Kellogg School of Management, as well as a master’s degree in computer science from the University of Minnesota and a bachelor’s degree in mechanical engineering from the Indian Institute of Technology in New Delhi.

ABOUT SECURIAN FINANCIAL

To be confident in your financial future, you need to trust the strength and commitment of the companies you choose to work with. For more than 145 years, the Securian Financial family of companies has been developing innovative insurance and retirement solutions to meet the evolving needs of individuals, families and businesses. Offered through partnerships with employers, financial professionals and affinity groups, our products help bring peace of mind to more than 23 million customers throughout the United States and Canada. We are trusted by our partners and customers to fulfill our purpose of helping to build secure tomorrows. For more information about Securian Financial, visit securian.com or follow us on Facebook, Instagram or LinkedIn.

Securian Financial is the marketing name for Securian Financial Group, Inc., and its subsidiaries. Insurance products are issued by its subsidiary insurance companies, including Minnesota Life Insurance Company and Securian Life Insurance Company, a New York authorized insurer.

2026 JUN 01 (NewsRx) — By a News Reporter-Staff News Editor at NewsRx Policy and Law Daily — Investigators publish new report on Legal Issues – Law and the Biosciences. According to news reporting originating in Washington, District of Columbia, by NewsRx journalists, research stated, “Whether life insurers should be able to consider genetic information during underwriting is a long-standing debate often characterized by strong opinions on both sides. Insurers push for full access to applicants’ genetic information, and consumer advocates often call for a ban on insurer use of the information.”

The news reporters obtained a quote from the research from the National Institutes of Health, “Both sides employ concepts of fairness and discrimination in supporting their position. This article considers the concept of actuarial fairness, where individuals are expected to pay for the risks they bring to an insurance pool. Currently, law and policy adopting this standard most often take a deferential approach, allowing insurers to utilize genetic information with wide latitude. This article takes seriously a middle-ground approach, broadly labeled as actuarial utility.”

According to the news reporters, the research concluded: “Building from prior literature examining this issue, this article proposes a framework US policy can adopt to assist in the assessment of the actuarial utility of genetic information with a particular focus on emerging genetic technologies.”

For more information on this research see: Taking actuarial fairness seriously: what is required for the ethical use of genetics in insurance? Journal of Law and the Biosciences, 2026;13(1). Journal of Law and the Biosciences can be contacted at: Oxford Univ Press, Great Clarendon St, Oxford OX2 6DP, England.

Our news correspondents report that additional information may be obtained by contacting Benjamin E. Berkman, Dept. of Bioethics, National Institutes of Health, Washington, DC, United States. Additional authors for this research include Harisan Nasir, Leila Jamal, Chloe Connor and Anya E. R. Prince.

The direct object identifier (DOI) for that additional information is: https://doi.org/10.1093/jlb/lsag017. This DOI is a link to an online electronic document that is either free or for purchase, and can be your direct source for a journal article and its citation.

The publisher of the Journal of Law and the Biosciences can be contacted at: Oxford Univ Press, Great Clarendon St, Oxford OX2 6DP, England.

(Our reports deliver fact-based news of research and discoveries from around the world.)

NEW YORK–(BUSINESS WIRE)–

26North Reinsurance Holding Company (“26North Re”) today announced that it has entered into a definitive agreement to acquire 100% of Independent Insurance Group, LLC (“Independent Group”), which operates Independent Life Insurance Company (“Independent Life”), the only carrier exclusively dedicated to issuing structured settlement annuities for personal injury claimants and their families.

The acquisition marks 26North Re’s entry into the U.S. insurance market and establishes its first onshore platform, complementing its existing Bermuda- and Cayman-domiciled operations. Independent Life will continue to operate under its existing brand following the close of the transaction, preserving the relationships and service standards that settlement planners and their clients rely on. 26North Re intends to build on that foundation, backing the business with long-term capital and proprietary asset origination to accelerate growth.

“This partnership will strengthen Independent Life’s leading franchise and provide the resources to enable consistent competitive pricing for settlement planners and claimants. For the people those settlements serve, 26North Re’s backing reinforces the certainty they have always counted on,” said 26North Senior Partner Cole Charnas. “We look forward to working alongside the management team on the next phase of the company’s expansion.”

With this transaction, 26North Re enters the structured settlement market, a specialized segment of the U.S. insurance industry in which long-dated liabilities, rigorous underwriting standards and disciplined asset management are prerequisites for all participants.

“Joining 26North Re gives Independent Life access to institutional-scale capabilities. Under 26North’s stewardship, we are positioned to serve more clients, in more markets with greater confidence than ever before,” said Independent Group CEO Donald Herrema.

The transaction is subject to customary regulatory approvals, including review by applicable state insurance departments.

RBC Capital Markets is serving as financial advisor to 26North Re and Kirkland & Ellis LLP is serving as legal counsel. Piper Sandler & Co. is acting as exclusive financial advisor to Independent Group and Mayer Brown LLP is acting as legal counsel.

ABOUT 26NORTH REINSURANCE HOLDING COMPANY

Founded in 2022, 26North Re has approximately $13 billion in assets on a pro forma basis, including multiple reinsurance transactions with high-quality, industry-leading ceding partners. The company leverages long-term capital, prudent risk controls and 26North Partners LP’s asset management capabilities. 26North Re helps protect the long-term financial security of more than 100,000 policyholders across the United States.

ABOUT 26NORTH PARTNERS LP

26North Partners LP is an integrated, multi-asset-class investment platform founded by Josh Harris in 2022. The firm manages approximately $37 billion across private equity, private credit, insurance and reinsurance strategies, bringing flexible capital solutions and distinct capabilities to the middle market.

26North Private Equity deploys capital across buyouts, carve-outs and structured equity. 26North Private Credit primarily invests in direct lending, private asset-backed finance and commercial real estate lending.

The firm’s insurance business serves clients with disciplined asset-liability management and access to proprietary, privately originated assets.

The 26North team brings decades of experience managing third-party capital to help clients achieve their financial goals while making a lasting impact on the communities in which they operate.

Founded by insurance company experts, the Independent Group is a forward-thinking enterprise whose complementary product and service companies improve outcomes for all structured settlement stakeholders. Independent Life, its underwriting division, is dedicated to providing structured settlement solutions, including annuities, to serve the needs of injured parties, their families and advocates. With its unique profile and ambitious vision for the structured settlement industry, Independent Life has attracted world-class partners, such as Hannover Re USA, to support its growth and guarantees.

Three Homegrown Leaders Elevated to Senior Management Committee Roles, Reflecting Depth of Lincoln’s Internal Talent Pipeline and Commitment to Strategic Execution

RADNOR, Pa.–(BUSINESS WIRE)–

Lincoln Financial (NYSE: LNC) today announced the promotion of three senior leaders to its Senior Management Committee (SMC): Darrel Tedrow as Executive Vice President, President of Life Insurance and Retail Shared Services; Curtis Chesney as Executive Vice President, President of Annuities; and Paul Spurr as Executive Vice President, Chief Risk Officer and Chief Actuary. All three report directly to Ellen Cooper, Chairman, President and CEO. These appointments are the direct result of Lincoln’s deliberate, multi-year investment in developing its next generation of executive leaders from within the organization.

This announcement also marks a structural evolution in the leadership of the company’s Life Insurance and Annuity businesses. Each business will now have a dedicated President reporting to Ellen Cooper. This decision reflects the significant strategic realignment currently underway in both franchises — each pursuing a distinct strategy with nuanced competitive dynamics, product sets, distribution landscapes, and capital considerations. The scope and complexity of the work at this stage in each business’s transformation requires dedicated executive focus.

Darrel Tedrow joined Lincoln 20 years ago and has been central to the strategic realignment of the company’s Life Insurance business in recent years, serving as President of Life since 2024. In his expanded role, Tedrow will continue to lead the Life business while also assuming executive oversight of operations and shared services functions that support the company’s Retail businesses. His mandate includes delivering on financial and growth objectives — including improving the free‑cash‑flow profile of the business — advancing product strategy, strategically partnering and collaborating with Lincoln’s world-class distribution team, and ensuring a leading customer experience. He brings both the strategic perspective and operational rigor this role demands.

Curtis Chesney brings 17 years of Lincoln experience to his new role leading the Annuity organization. Most recently serving as CFO of Lincoln’s Annuity business, Chesney brings a command of the products, economics, and competitive dynamics of this market. He also previously led Corporate Financial Planning and Analysis across all of Lincoln’s business segments, giving him an enterprise-wide financial perspective. In his new role, Chesney is responsible for delivering on financial and growth objectives, overseeing product strategy and in-force management and ensuring a high-quality experience for customers and advisors across all distribution channels. He will lead the business through its continued diversification toward more spread-based products designed to produce more stable cash flows and reduce market sensitivity over time, while maintaining disciplined risk management aligned to Lincoln’s long-term financial position.

Paul Spurr has been with Lincoln for more than two decades, serving in progressively senior leadership roles across finance, risk, and actuarial functions. By bringing risk and actuarial under a single leader, Lincoln is strengthening its well-established risk management foundation while creating a more integrated, enterprise-wide approach to oversight. Spurr’s deep expertise across both disciplines positions him to lead this expanded mandate. In this role, he is responsible for advancing Lincoln’s risk management framework, overseeing the company’s risk profile, and ensuring risk considerations are embedded in capital allocation, product strategy, and business planning. He also leads actuarial practices across valuation, reserving, and pricing, further enhancing discipline and consistency across the organization.

These promotions coincide with the planned retirements of Brian Kroll, EVP and President of Retail Life and Annuity Solutions, and Andy Rallis, EVP and Chief Risk Officer — both effective June 1, 2026. Kroll and Rallis each joined Lincoln at pivotal moments for the company and delivered on clear mandates to advance the company’s near-term strategic objectives while also developing future executive leadership talent. Both have been working closely with their successors to ensure a seamless transition.

“These promotions reflect the incredible depth of talent we have developed at Lincoln and our commitment to thoughtful, deliberate succession planning,” said Cooper. “Darrel, Curtis and Paul each bring deep institutional knowledge, proven leadership, and a track record of results that give me tremendous confidence in our path forward. It is genuinely exciting to see leaders of this caliber step into expanded roles, and I look forward to the energy they will bring to our Senior Management Committee as we continue to lead our talented workforce in executing on our strategy and delivering for our customers, partners, and shareholders.”

“We also want to recognize and thank Brian Kroll and Andy Rallis for their significant contributions to Lincoln,” Cooper continued, “I am deeply grateful for their partnership, their leadership, and their commitment to our strategy and our people — and I wish them both the very best in their well-earned retirements.”

About Lincoln Financial

Lincoln Financial helps people confidently plan for their vision of a successful financial future. As of December 31, 2025, approximately 17 million customers trust our guidance and solutions across four core businesses – annuities, life insurance, group protection, and retirement plan services. As of March 31, 2026, the company has $340 billion in end-of-period account balances, net of reinsurance. Headquartered in Radnor, Pa., Lincoln Financial is the marketing name for Lincoln National Corporation (NYSE: LNC) and its affiliates.

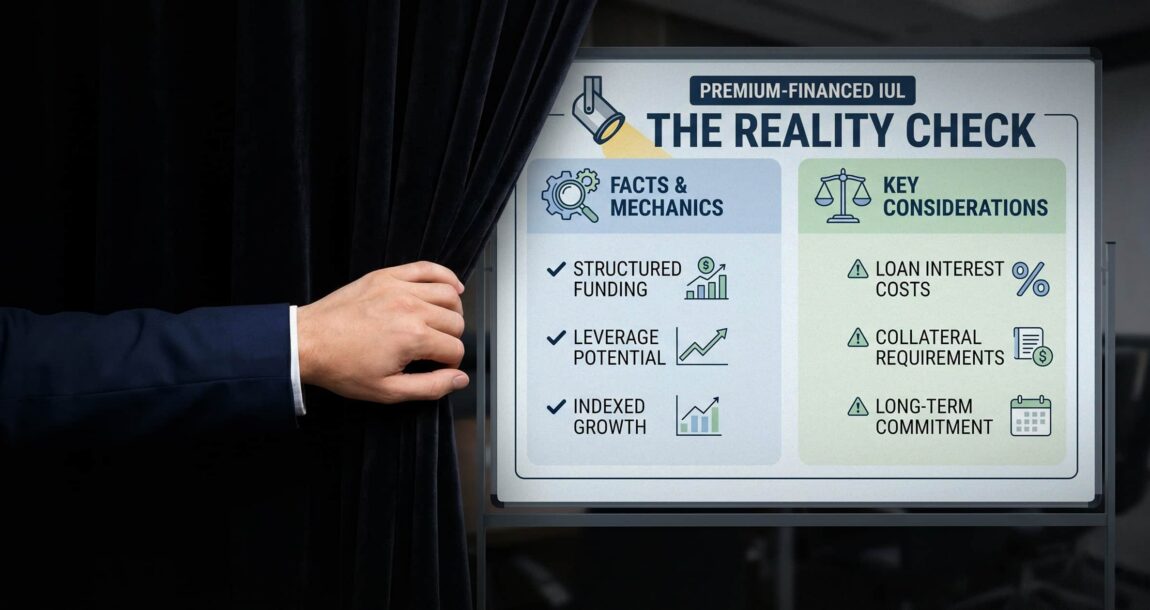

If you sell life insurance, you already know indexed universal life. You know the flexible premiums, the downside protection, the cash value tied to an index like the S&P 500, and a death benefit that can serve a family for decades.

Michael J. Rothman

What you may be less familiar with is what happens when a high net worth client uses borrowed money to fund that policy, a strategy known as premium financing, and why that strategy has become the subject of some of the most charged coverage in the insurance trade press in recent memory.

Here is the short version of how it works. A client with a significant estate-planning need, typically a projected estate tax liability of millions of dollars, takes out a loan from a third-party lender to fund the premiums on a large IUL policy. The policy is pledged as collateral, along with other personal assets. The client pays interest on the loan, typically out of pocket each year. The policy accumulates cash value over time, and the design assumes the cash value will eventually retire the loan principal, usually within 15 to 20 years.

What remains is a fully funded life insurance policy that provides a tax-advantaged death benefit to address the estate tax exposure the client sought to address in the first place. This is not a funding strategy for the average policyholder. It is a sophisticated planning approach for clients with complex balance sheets, illiquid assets and real, quantifiable estate-planning needs.

It is also a strategy that has recently drawn significant scrutiny. A Financial Industry Regulatory Authority arbitration panel ordered a former broker to pay $2.25 million to his client’s estate. The client’s family alleged that the broker “pushed” a premium-financed IUL arrangement on the client that exposed them to outsized risk, resulted in a “massive” commission to the agent and caused significant losses.

Cases such as this one, alongside a wave of critical trade coverage that frames premium-financed IULs as a commission-driven debt trap, put advisors in this space on the defensive. Some are pulling back from the strategy entirely. Others are struggling to respond to client questions shaped by negative headlines.

That pullback is understandable. It is also, in most cases, premature and short-sighted. The cases driving the negative coverage are real, but they are problems of execution and disclosure, not of the strategy itself. There is an important distinction between the two, and it is one every advisor who works with high net worth clients must clearly understand. With that context in mind, let’s address the three misconceptions doing the most damage right now.

Misconception 1: Premium-financed IUL Is “free insurance”

You have probably heard this framing. The idea is that the policy’s cash value growth eventually repays the loan, so the client gets coverage without effectively spending their own money. It is a catchy line. It is also completely wrong.

Clients pay interest on the loan, typically out of pocket, annually. That is a real, ongoing cost. Any advisor or client who believes that deferring or skipping loan interest carries no negative consequence is mistaken. In almost all premium-financed structures, the client pays interest out of pocket. Focusing on the small subset of cases where interest is never paid, without that context, is misleading and detracts from the strategy’s genuine value.

For clients using premium-financed IUL as an estate-planning tool, this framing misrepresents the actual rationale for planning. These are high-net-worth individuals with projected estate tax liability or significant liquidity needs who are making a deliberate cost-benefit decision. Many hold highly illiquid assets, and life insurance addresses the worst-case outcome at death in a way few other tools can. The relevant question is whether the interest cost is justified by the estate tax exposure being addressed and whether it compares favorably with out-of-pocket premiums that are often many times higher. A straightforward presentation covers the loan amount, the interest rate, the alternative premium cost without financing, and the estate-planning needs the structure is designed to meet. Complexity is not the problem at the high-net-worth level. Context is.

Misconception 2: IUL illustrations are uniquely unreliable

Critics who argue that illustrated IUL returns are unlikely to be realized under real market conditions often do so without applying the same standard to the rest of the product universe. That inconsistency matters.

IUL illustrations are governed by Actuarial Guideline 49, a regulatory framework that grounds assumptions in historical index performance. That is not a marketing claim; it is a regulatory requirement. Meanwhile, whole life dividend scales have declined steadily over the past two decades, yet that is rarely described as a systemic product problem. Variable universal life policies can illustrate returns of 8% or more without attracting the same scrutiny. If the standard is going to be applied to IUL, intellectual honesty requires applying it across the board.

For clients using premium-financed IUL in an estate-planning context, the success criteria differ from those used in a retirement-income design. An estate-planning strategy is evaluated against the death benefit, its cost and the efficiency of addressing the estate tax liability through the policy versus alternatives. Conflating that objective with a retirement accumulation narrative, then criticizing the illustration for not meeting retirement income benchmarks, produces conclusions that do not apply to the strategy being evaluated.

Misconception 3: Early underperformance equals policy failure

This may be the most consequential misunderstanding in circulation right now.

No life insurance policy is designed to be evaluated in year five. This is especially true for estate-planning strategies, where the policy’s purpose is to deliver a death benefit that addresses estate tax exposure at the point of wealth transfer. The relevant measuring sticks are whether the death benefit is in force and whether the need still exists. Given market conditions over the past 10 to 15 years, most IUL policies have outperformed their illustrated projections. Arguments about future failure are speculation, not evidence.

When early-year performance does not match the illustrated projections, the correct response is a review conversation: examine interest rate changes, index performance and the client’s financial picture, then adjust the design where appropriate. Clients who find themselves strained because they stopped paying interest and can no longer meet collateral requirements are not victims of a flawed product. They are experiencing the consequences of an execution problem that almost always stems from inadequate expectation-setting at the point of sale.

The real differentiator: How you present, not what you sell

Complaints about the premium-financed IUL space rarely stem from the strategy itself. They stem from the gap between what clients believed they were told to expect and what they experienced, and, more fundamentally, from a disconnect with the coverage’s original purpose. In most cases, the underlying need for life insurance has not changed.

Estate planning is where premium-financed IUL does its most consequential work. A properly structured policy can preserve assets, create a tax-advantaged transfer mechanism, and provide certainty around an estate tax liability that would otherwise significantly reduce what the family passes on. That outcome deserves to be communicated clearly and in the client’s terms.

The cases making headlines, including the FINRA arbitration mentioned earlier in this article, share a common thread: a breakdown in disclosure, expectation-setting and comprehension at the point of sale. Those are execution failures. The strategy they involve is not inherently broken. Understanding that distinction is the starting point for every financial professional who wants to serve high net worth clients in this space with confidence and integrity.