NEW YORK–(BUSINESS WIRE)–

KBRA releases commentary following the recent publication of the Columbia Business School’s Rating Without Market Discipline paper, which raises important questions regarding the growth of private ratings in U.S. life insurer portfolios and the interaction between ratings and regulatory capital. The paper concludes that privately rated bonds understate credit risk, experience higher subsequent impairment rates, and contribute to lower required capital than comparable publicly rated bonds.

This KBRA research reviews the paper’s methodology and its interpretation of the evidence. Our objective is not to argue that private ratings should be exempt from scrutiny. Rather, it is to help fixed income investors evaluate whether the evidence presented in the paper supports the breadth of its conclusions—which, we believe, they do not. Put differently, the paper’s rhetorical emphasis is on systemic risk, policyholder welfare, widespread rating inflation, and the absence of market discipline, while its principal quantitative estimate is a hypothetical modeled capital adjustment that is insignificant relative to the financial resources of the industry.

Key Takeaways

Even if one accepts the entirety of the paper’s analytical assumptions and inferential steps as valid, the authors’ own illustrative capital exercise implies approximately $4 billion of additional required capital for the entire U.S. life insurance industry.

Based on NAIC’s 2024 Life RBC Statistics, that amount represents roughly 0.5% of industry total adjusted capital (TAC), approximately 0.6% of industry surplus, and less than 0.1% of invested assets. In other words, a small pro forma impact on the industry’s risk-based capital ratio (RBC) of approximately 38 RBC points (830% versus 868%).

That conclusion is considerably narrower and economically more modest than the impression conveyed by the paper’s title, abstract, and concluding discussion.

KBRA, one of the major credit rating agencies, is registered in the U.S., EU, and the UK. KBRA is recognized as a Qualified Rating Agency in Taiwan, and is also a Designated Rating Organization for structured finance ratings in Canada. As a full-service credit rating agency, investors can use KBRA ratings for regulatory capital purposes in multiple jurisdictions.

Variable universal life insurance is known for the flexibility it offers clients. According to first-quarter sales numbers from Wink, Inc., clients are embracing the product.

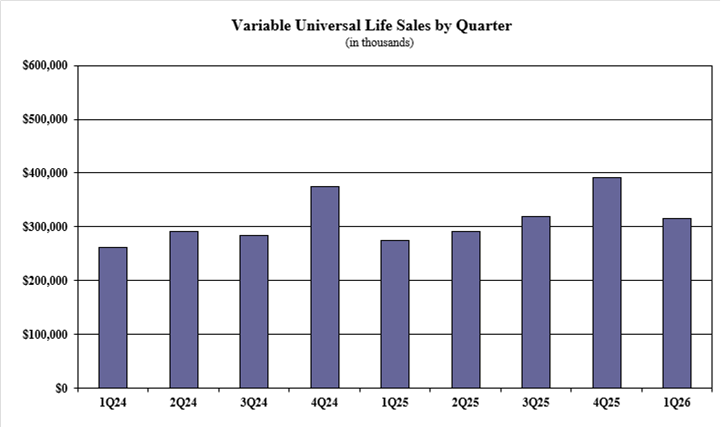

VUL sales were up 15.1% over Q1 2025, Wink reported in its latest Sales & Market Report. Sales began percolating during the fourth quarter, with VUL up 4.3% over the prior-year quarter and up 22.4% over Q3.

Sales are slowest during Q1 and strongest at the end of the year. Total VUL sales for the first quarter were $316.1 million, down 19.1% quarter-over-quarter.

“The market has been on the uptick since the beginning of April,” said Sheryl Moore, CEO of Wink, Inc. and Moore Market Intelligence. “This translates to improved sales of variable UL.”

VUL is a permanent life insurance policy that combines a death benefit with an investment component. Policies can be customized with specific riders to provide coverage for needs such as long-term care.

Items of interest in the VUL market included Prudential retaining the No. 1 ranking in sales, with a 36.2% market share; Pacific Life Companies, Nationwide, RiverSource Life and John Hancock completed the top five, respectively.

Pruco Life’s PruLife Custom Premier II was the No. 1 selling VUL product, for all channels combined, for the quarter. The top primary pricing objective for sales this quarter was cash accumulation, capturing 63.4% of sales. The average VUL target premium for the quarter was $23,161, a decline of nearly 10% from the prior quarter.

Overall life sales up 8%

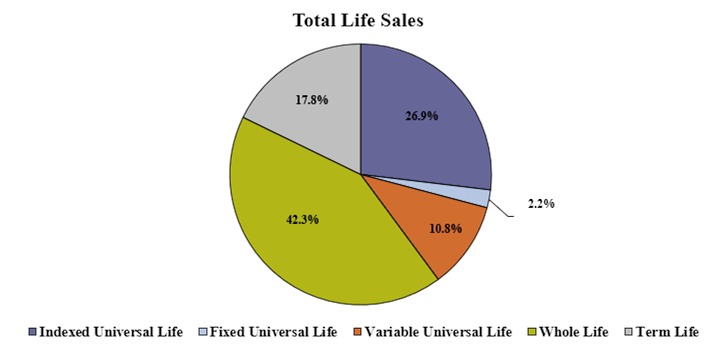

All life insurance sales for the first quarter were more than $2.9 billion, down 9.7% compared to the previous quarter and up 8.1% compared to the same period last year. All life sales include fixed universal life, indexed UL, variable UL, indexed whole life, whole life and term life product sales.

Noteworthy highlights for total life insurance sales of all products in the first quarter included Prudential ranking as No. 1 in overall sales for all life insurance sales, with a market share of 5.6%. Americo’s Eagle Select, a whole life product, was the No. 1 selling product for all life insurance sales, for all channels combined, for the quarter.

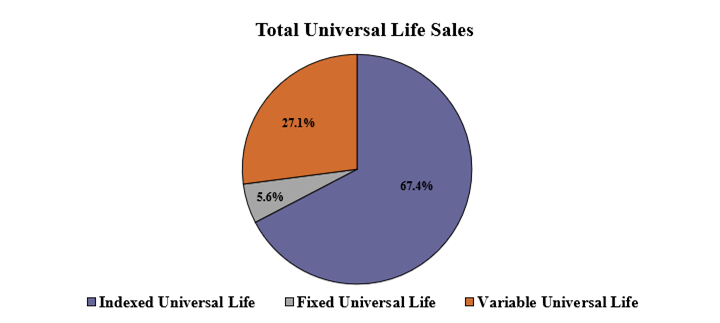

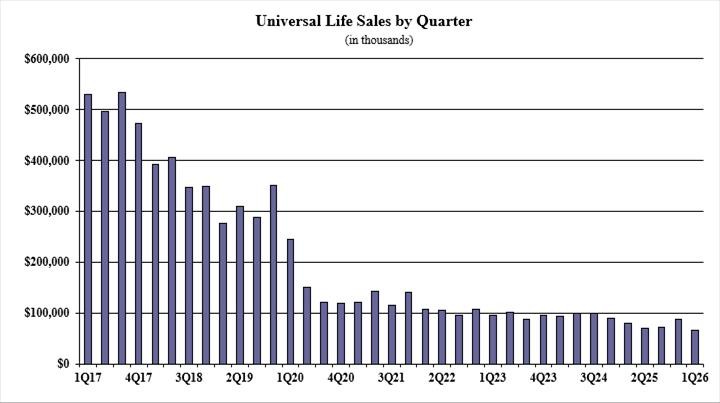

All universal life sales for the first quarter were $1.1 billion, down 16% compared to the previous quarter and up 4.3% compared to the same period last year. All universal life sales include fixed UL, indexed UL and variable UL product sales.

Noteworthy highlights for all universal life sales in the first quarter included Prudential ranking as No. 1 in overall sales for all universal life products, with a market share of 11.2%. Life Insurance Co. of the Southwest’s FlexLife, an indexed universal life product, was the No. 1 selling product for all universal life sales, for all channels combined, for the quarter.

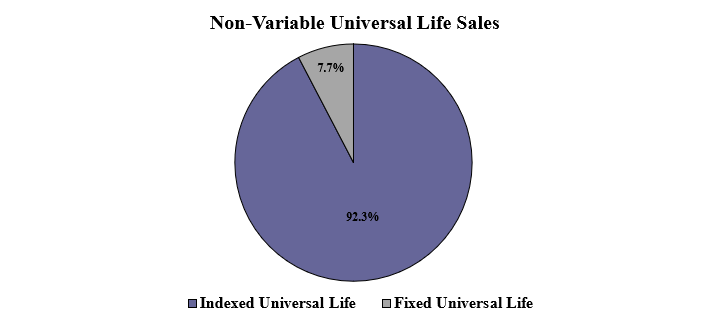

Non-variable universal life sales for the first quarter were $851.9 million, down 15.2% when compared to the previous quarter and up less than 1% compared to the same period last year. Non-variable universal life sales include both fixed UL and indexed UL product sales.

Noteworthy highlights for total non-variable universal life sales in the first quarter included National Life Group retaining the No. 1 overall sales ranking for non-variable universal life sales, with a market share of 13.8%. Life Insurance Co. of the Southwest’s FlexLife, an indexed universal life product, was the No. 1 selling product for non-variable universal life sales, for all channels combined, for the quarter.

Fixed universal life sales for the first quarter were $65.2 million, down 25.9% compared to the previous quarter and down 18% compared to the same period last year.

Items of interest in the fixed UL market included Nationwide retaining its No. 1 ranking in fixed universal life sales, with a 22.8% market share; Pacific Life Companies, John Hancock, Protective Life Companies and Penn Mutual completed the top five, respectively.

Nationwide’s Nationwide CareMatters II was the No. 1 selling fixed universal life insurance product, for all channels combined, for the quarter. The top primary pricing objective of no lapse guarantee captured 33.0% of sales. The average fixed UL target premium for the quarter was $6,826, a decline of more than 22% from the prior quarter.

“Universal life sales have never been this low,” Moore said. “It is just getting more difficult to justify the sales of these products, when indexed life has a relatively stronger value proposition.”

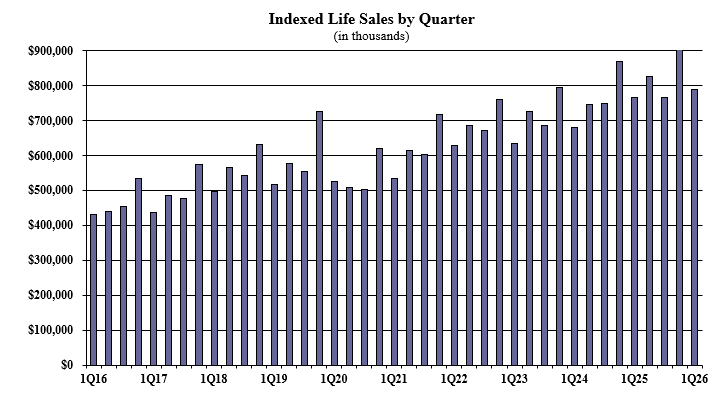

Indexed life sales for the first quarter were $789.5 million, down 14% compared with the previous quarter, and up 2.8% compared to the same period last year. Indexed life sales include both indexed UL and indexed whole life.

Items of interest in the indexed life market included National Life Group retaining its No. 1 ranking in indexed life sales, with a 14.7% market share; Pacific Life Companies, John Hancock, Nationwide, and Fidelity and Guaranty Life rounded out the top five, respectively.

Life Insurance Co. of the Southwest’s FlexLife was the No. 1 selling indexed life insurance product, for all channels combined, for the quarter. The top primary pricing objective for sales in the quarter was cash accumulation, capturing 74.7% of sales. The average indexed life target premium for the quarter was $12,922, a decline of nearly 3% from the prior quarter.

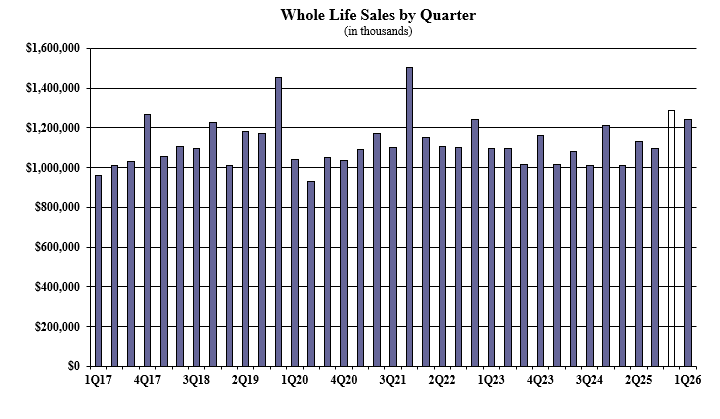

Whole life first quarter sales were over $1.2 billion, down 3.6% compared with the previous quarter, and up 22.6% compared to the same period last year. Items of interest in the whole life market included the top primary pricing objective of final expense, capturing 72.4% of sales. The average premium per whole life policy for the quarter was $3,860, a decline of more than 19% from the prior quarter.

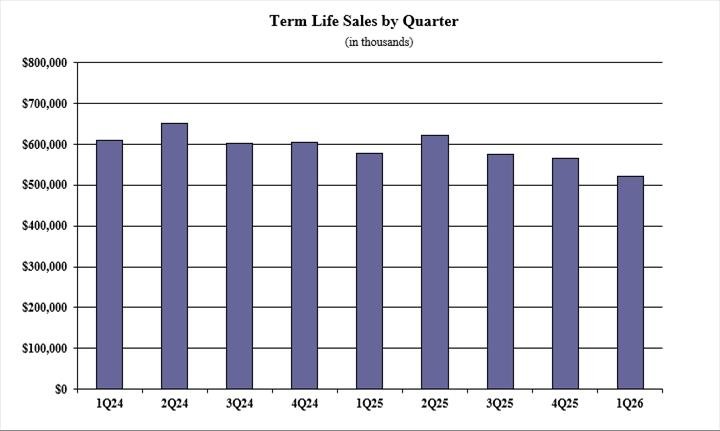

Term life first-quarter sales were $521.8 million, down 7.6% when compared with the previous quarter and down 9.7% compared to the same period last year.

Items of interest in the term life market include Prudential ranking as No. 1 in term life sales, with a 6.5% market share. Pacific Life Companies, Protective Life Companies, Corebridge Financial, and National Life Group completed the top five, respectively.

Protective Life Classic Choice Term 20 was the No. 1 selling term life insurance product, for all channels combined, for the quarter. The average annual term life premium per policy reported for the quarter was $1,905, a decline of nearly 29% from the previous quarter.

Wink now reports sales on all annuity lines of business, as well as all life insurance product lines.

NEW YORK–(BUSINESS WIRE)–

KBRA releases research on the National Association of Insurance Commissioners (NAIC) private letter ratings (PLR) review process. In August 2024, the NAIC passed an amendment that granted the Securities Valuation Office (SVO) the ability to review and challenge credit ratings that it does not believe are a reasonable measure of risk for regulatory purposes (the Discretion Amendment). Although the Discretion Amendment’s original January 2026 implementation has been delayed, it has focused attention on PLRs, the regulatory treatment of rated private assets, and the potential implications for U.S. life insurers’ risk-based capital (RBC) positions. KBRA views the potential impact of the Discretion Amendment through a measured analytical lens that considers the likely scope of reviews, the security-specific nature of potential outcomes, the distinction between required capital and statutory capital impairment, and the broader capital management tools available to insurers.

Key Takeaways

PLRs are not synonymous with private credit. While private credit represents an important part of the PLR market, PLRs may be associated with a range of asset types and transaction structures. The potential regulatory capital impact of a PLR review therefore depends on the specific security, its structure, collateral, rating level, and resulting NAIC designation.

Potential capital effects are likely to be security specific. KBRA expects the PLR review process to focus on individual securities or groups of securities with identified analytical or regulatory concerns. As a result, any RBC impact would likely depend on the size, rating category, NAIC designation, and insurer-level concentration of the affected holdings.

RBC sensitivity should be distinguished from economic loss. A change in statutory bond risk charges may increase authorized control level RBC (ACL), thereby lowering an RBC ratio if total adjusted capital (TAC) is unchanged. That outcome is different from a realized credit loss, impairment, or reduction in statutory surplus.

Company-level analysis should incorporate more than statutory RBC metrics. Insurer financial strength also depends on, among other things, asset-liability management, investment governance, earnings capacity, reinsurance arrangements, enterprise capital resources, and potential management actions.

For all credit ratings, whether published or unpublished, KBRA applies the same analytical approach, methodologies, rating scales, and controls through uniform rating committee processes and surveillance practices (see Unpublished Ratings: Same Standards, Different Distribution). The only distinction is in how the rating and associated reports are disseminated: For public ratings, this is accomplished through the KBRA website, while private ratings are distributed to the engaging entity through a virtual data room. KBRA publishes an annual Global Rating Stability and Transition Study, incorporating both published and private credit ratings, which indicates stability across the ratings universe. Other KBRA research has highlighted consistent performance for published and unpublished ratings (see Private Credit SF: How KBRA Ratings Stack Up).

KBRA, one of the major credit rating agencies, is registered in the U.S., EU, and the UK. KBRA is recognized as a Qualified Rating Agency in Taiwan, and is also a Designated Rating Organization for structured finance ratings in Canada. As a full-service credit rating agency, investors can use KBRA ratings for regulatory capital purposes in multiple jurisdictions.

Rate enhancements also made to flagship traditional variable annuity product suite

LANSING, Mich.–(BUSINESS WIRE)– Jackson National Life Insurance Company® (Jackson®), the main operating subsidiary of Jackson Financial Inc.1 (NYSE: JXN), today launched Jackson Market Link Pro® 4 (JMLP4) and Jackson Market Link Pro Advisory® 4 (JMLPA4), further strengthening Jackson’s suite of registered index-linked annuities (RILAs). JMLP4 (commission-based) and JMLPA4 (fee-based) provide clients the potential to grow assets before and during retirement while offering different degrees of protection, including full principal protection, against unexpected market events. Additionally, Jackson recently made improvements to its flagship traditional variable annuity (VA) product suite, delivering enhanced value and flexibility to financial professionals and their clients.

“Jackson continues our focus on expanding retirement planning options for financial professionals and their clients with these enhancements to our RILA and traditional VA product suites,” said Alison Reed, EVP, Head of Distribution, Jackson National Life Distributors LLC (JNLD), the marketing and distribution business of Jackson. “By being the first in the industry to introduce the Dow Jones Industrial Average (DJIA) as an index option with a RILA, offering clients the ability to add funds to an existing contract and adding a guaranteed cap crediting method that locks in rates for six premium years, we’re empowering clients with more choice and confidence in their investment strategies.”

JMLP4 and JMLPA4 enhancements include the following:

DJIA Index Option: The addition of the DJIA as an index option provides clients with another avenue to invest their funds in accordance with their unique values and investment preferences and is now available alongside the S&P 500, Russell 2000, Nasdaq-100, MSCI EAFE and MSCI Emerging Markets. Jackson will not restrict which index options can be selected with each crediting method or protection option, enabling clients to adjust their allocations without triggering unwanted tax consequences and invest in what aligns with their priorities2.

Flexible Premiums: JMLP4 and JMLPA4 are the first RILA products offered at Jackson designed to allow flexible premiums. This feature allows clients to add funds to an existing contract without submitting a new application, providing a more streamlined and convenient way to invest additional assets.

Guaranteed Cap Crediting Method3: Clients can lock in a cap rate removing any concern with what the renewal rate will be for the entire guarantee period, which is the first six premium years. This feature is only available on the 1- and 3-year terms with a 10% buffer.

Full or Partial Performance Lock: With a performance lock, clients can choose to lock in all (full performance lock) or a portion (partial performance lock) of their interim value at any point during the index account option term. In practice, the value at the lock-in point moves to a performance lock holding account where amounts earn a declared rate of interest until the next premium allocation anniversary4, when it can be reallocated.

Rate Enhancement Option5: At contract issue, for an additional charge, consumers can elect a rate enhancement option on all available terms, crediting methods, and protection options, providing the opportunity for greater growth.

In addition to these enhancements, Jackson’s JMLP RILA suite offers the following competitive features:

Full Principal Protection: The JMLP4 suite offers a 100% buffer (30% buffer in New York) protection option for the 1-year cap, 3-year cap, 6-year cap and 1-year performance trigger crediting methods, in addition to 10% and 20% options. The level of protection depends on the crediting method selected6.

Flexible Index Account Option Terms: Jackson offers 1-year, 3-year and 6-year index account option terms7. Any gains or losses in the tracked index(es) (described above) are calculated at the end of the term, and the contract value is adjusted accordingly.

Multiple Crediting Methods: Jackson offers a diverse menu of crediting methods that allows consumers the ability to customize their contract both in terms of growth potential and protection level. In addition to the guaranteed cap crediting method, Jackson offers three additional crediting methods – cap, performance boost8 and performance trigger.

Enhancements to Extended Care9 and Terminal Illness10 Waivers: Beginning with JMLP4, there is no limit on the frequency of withdrawals that can be made utilizing these waivers and no cap on the amount of money that can be withdrawn.

Legacy and Cost Control: Through the built-in death benefit11 — available at no additional charge — clients can help protect their retirement assets against market downturns while providing a legacy for beneficiaries. Additionally, with no annual contract fees12, more investable assets remain in clients’ contracts.

Jackson also recently announced the following enhancement to its suite of VAs as well as a series of fund changes.

Guaranteed Withdrawal Rates: Jackson has increased Single Life and Joint Life Guaranteed Annual Withdrawal Amount Percentages (GAWA%) across multiple options within its Flex Suite of living benefits and New York Flex Suite of living benefit options, including Flex Core, Flex Net Core, Flex DB Core, and Flex Plus.

“As market conditions and client needs continue to evolve, Jackson is enhancing our industry leading variable annuity lineup to provide financial professionals and their clients with more options and flexibility,” said Brian Sward, EVP, Head of Product Solutions, JNLD. “These enhancements reinforce our commitment to delivering value across a broad range of market environments and reflect Jackson’s ongoing dedication to providing products that support personalized strategies and long-term financial success.”

Financial professionals who would like to learn more about Jackson’s recent product enhancements can contact the company at 1-800-711-7397, connect with their local wholesaler or visit http://www.jackson.com/financial-professional.

ABOUT JACKSON

Jackson® (NYSE: JXN) is committed to helping clarify the complexity of retirement planning—for financial professionals and their clients. Through our range of annuity products, financial know-how, history of award-winning service* and streamlined experiences, we strive to reduce the confusion that complicates retirement planning. We take a balanced, long-term approach to responsibly serving all our stakeholders, including customers, shareholders, distribution partners, employees, regulators and community partners. We believe by providing clarity for all today, we can help drive better outcomes for tomorrow. For more information, visit www.jackson.com.

*SQM (Service Quality Measurement Group) Call Center Awards Program for 2004 and 2006-2025. (Criteria used for Call Center World Class FCR Certification is 80% or higher of customers getting their contact resolved on the first call to the call center (FCR) for three consecutive months or more.)

Jackson® is the marketing name for Jackson Financial Inc., Jackson National Life Insurance Company® (Home Office: Lansing, Michigan) and Jackson National Life Insurance Company of New York® (Home Office: Purchase, New York).

SAFE HARBOR STATEMENT

The information in this press release contains forward-looking statements about future events and circumstances and their effects upon revenues, expenses and business opportunities. Generally speaking, any statement in this release not based upon historical fact is a forward-looking statement. Forward-looking statements can also be identified by the use of forward-looking or conditional words, such as “could,” “should,” “can,” “continue,” “estimate,” “forecast,” “intend,” “look,” “may,” “expect,” “believe,” “anticipate,” “plan,” “predict,” “remain,” “future,” “confident” and “commit” or similar expressions. In particular, statements regarding plans, strategies, prospects, targets and expectations regarding the business and industry are forward-looking statements. They reflect expectations, are not guarantees of performance and speak only as of the dates the statements are made. We caution investors that these forward-looking statements are subject to known and unknown risks and uncertainties that may cause actual results to differ materially from those projected, expressed, or implied. Other factors that could cause actual results to differ materially from those in the forward-looking statements include those reflected in Part I, Item 1A. Risk Factors and Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations in our Annual Report on Form 10-K for the year ended December 31, 2025, as filed with the U.S. Securities and Exchange Commission (the “SEC”) on February 24, 2026, and elsewhere in the Company’s reports filed with the SEC. Except as required by law, Jackson Financial Inc. does not undertake to update such forward-looking statements. You should not rely unduly on forward-looking statements.

GENERAL DISCLOSURES

Jackson, its distributors, and their respective representatives do not provide tax, accounting, or legal advice. Any tax statements contained herein were not intended or written to be used and cannot be used for the purpose of avoiding U.S. federal, state, or local tax penalties. Tax laws are complicated and subject to change. Tax results may depend on each taxpayer’s individual set of facts and circumstances. You should rely on your own independent advisors as to any tax, accounting, or legal statements made herein.

Annuities are long-term, tax deferred vehicles designed for retirement and are insurance contracts. Variable annuities and registered index-linked annuities involve investment risks and may lose value. Earnings are taxable as ordinary income when distributed. Individuals may be subject to a 10% additional tax for withdrawals before age 59½ unless an exception to the tax is met.

Guarantees are backed by the claims-paying ability of Jackson National Life Insurance Company or Jackson National Life Insurance Company of New York. They are not backed by the broker/dealer from which this annuity contract is purchased, by the insurance agency from which this annuity contract is purchased or any affiliates of those entities, and none makes any representations or guarantees regarding the claims-paying ability of Jackson National Life Insurance Company or Jackson National Life Insurance Company of New York.

This material is authorized for use only when preceded or accompanied by the current contract prospectus. Before investing, investors should carefully consider the investment objectives and risks of the registered index-linked annuity. This and other important information is contained in the current contract prospectus at Jackson.com/ProspectusJMLP4NY for the Jackson Market Link Pro 4 (New York) prospectus, Jackson.com/ProspectusJMLP4 for the Jackson Market Link Pro 4 prospectus, Jackson.com/ProspectusJMLPA4NY for the Jackson Market Link Pro Advisory 4 (New York) prospectus or Jackson.com/ProspectusJMLPA4 for the Jackson Market Link Pro Advisory 4 prospectus.

The “S&P 500®” and the “Dow Jones Industrial Average®” (the “Indices”) are products of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”) and have been licensed for use by Jackson National Life Insurance Company (“Jackson”) and Jackson National Life Insurance Company of New York (“Jackson of NY”). S&P 500®, SPX®, SPY®, US 500, The 500, iBoxx®, iTraxx®, CDX®, The Dow®, DJIA®, and Dow Jones Industrial Average® are trademarks of S&P Global, Inc. or its affiliates (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by Jackson and Jackson of NY. Jackson’s products are not sponsored or sold by SPDJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such products, nor do they have any liability for any errors, omissions, or interruptions of the indices.

The Jackson Market Link Pro Suite has been developed solely by Jackson National Life Insurance Company and Jackson National Life Insurance Company of New York. These products are not in any way connected to or sponsored, endorsed, sold or promoted by the London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). FTSE Russell is a trading name of certain of the LSE Group companies.

All rights in the Russell® 2000 (the “Index”) vest in the relevant LSE Group company which owns the index. Russell® is a trademark of relevant LSE Group company and is used by other LSE Group company under license.

The index is calculated by or on behalf of FTSE International Limited or its affiliate, agent or partner. The LSE Group does not accept any liability whatsoever to any person arising out of (a) the use of, reliance on or any error in the index or (b) investment in or operation of the Jackson Market Link Pro Suite. The LSE Group makes no claim, prediction, warranty or representation as to the results to be obtained from the Jackson Market Link Pro Suite or the suitability of the Index for the purpose to which it is being put by Jackson National Life Insurance Company and Jackson National Life Insurance Company of New York.

The Product referred to herein is not sponsored, endorsed, or promoted by MSCI, and MSCI bears no liability with respect to any such Products or any index on which such Products are based. The Contract contains a more detailed description of the limited relationship MSCI has with Jackson National Life Insurance Company and Jackson National Life Insurance Company of New York and any related Products.

Nasdaq®, Nasdaq-100®, Nasdaq-100 Index®, and NDX® are registered trademarks of Nasdaq, Inc. (which with its affiliates is referred to as the “Corporations”) and are licensed for use by Jackson National Life Insurance Company® (“Jackson”) and Jackson National Life Insurance Company of New York (“Jackson of NY”). The Product(s) have not been passed on by the Corporations as to their legality or suitability. The Product(s) are not issued, endorsed, sold, or promoted by the Corporations. THE CORPORATIONS MAKE NO WARRANTIES AND BEAR NO LIABILITY WITH RESPECT TO THE PRODUCT(S).

Registered index-linked annuities (contract form numbers ICC25 RILA310, ICC25 RILA310-CB1, ICC25 RILA312, ICC25 RILA312-CB1, ICC25 RILA315, ICC25 RILA315-FB1, ICC25 RILA317, ICC25 RILA317-FB1) are issued by Jackson National Life Insurance Company (Home Office: Lansing, Michigan) and in New York (contract form numbers RILA310NY, RILA310NY-CB1, RILA312NY, RILA312NY-CB1, RILA315NY, RILA315NY-FB1, RILA317NY, RILA317NY-FB1) by Jackson National Life Insurance Company of New York (Home Office: Purchase, New York) and distributed by Jackson National Life Distributors LLC, member FINRA. May not be available in all states and state variations may apply. These products have limitations and restrictions, including withdrawal charges or market value adjustments. Market value adjustments are not applied in New York. Jackson issues other annuities with similar features, benefits, limitations and charges. Discuss them with your financial professional or contact Jackson for more information.

VARIABLE ANNUITY DISCLOSURES

This material is authorized for use only when preceded or accompanied by the current contract prospectus and underlying fund prospectuses. Before investing, investors should carefully consider the investment objectives, risks, charges, and expenses of the variable annuity and its underlying investment options. This and other important information are contained in the current contract prospectus and underlying fund prospectuses. Please read the prospectuses carefully before investing or sending money.

On the contract anniversary on or immediately following the designated life’s attained age 59½, the for-life guarantee becomes effective provided: 1) the contract value is greater than zero and 2) the contract has not been annuitized. If the designated life is age 59½ on the effective date of the endorsement, then the for-life guarantee becomes effective on that date.

The latest income date allowed on variable annuity contracts is age 95, which is the required age to annuitize or take a lump sum.

Add-on benefits are available for an extra charge in addition to the ongoing fees and expenses of the variable annuity.

Variable annuities (contract form numbers VA775, VA775-CB1, VA775-RLC, ICC18 VA775, ICC18 VA775-CB1, ICC18 VA775-RLC, VA710, VA710-CB1, ICC19 VA710, ICC19 VA710-CB1, VA720, VA720-CB1, ICC19 VA720, ICC19 VA720-CB1, VA790, VA790-FB1, ICC17 VA790, ICC17 VA790-FB1, VA670, VA670-CB1, ICC19 VA670, ICC19 VA670-CB1, VA680, VA680-CB1, ICC19 VA680, ICC19 VA680-CB1, VA785, VA785-FB1, ICC18 VA785, ICC18 VA785-FB1) are issued by Jackson National Life Insurance Company (Home Office: Lansing, Michigan) and in New York (contract form numbers VA775NY, VA775NY-CB1, VA790NY, VA790NY-FB1, VA670NY, VA670NY-CB1, VA785NY, VA785NY-FB1) by Jackson National Life Insurance Company of New York (Home Office: Purchase, New York). Variable products are distributed by Jackson National Life Distributors LLC, member FINRA. These contracts have limitations and restrictions. Jackson issues other annuities with similar features, benefits, limitations, and charges. Discuss them with your financial professional or contact Jackson for more information.

Products and features may be limited by state availability, and/or your selling firm’s policies and regulatory requirements (including standard of conduct rules).

__________________________________

1 Jackson National Life Insurance Company is a wholly owned subsidiary of Jackson Financial Inc. Jackson Financial Inc. is a publicly traded company.

2 Investors are not buying shares of any stock or index and cannot invest directly in an index. The payment of dividends is not reflected in the index return.

3 Once the index account option value is removed from an index account option with a guaranteed cap crediting method, it cannot be reallocated into a new or existing guaranteed cap crediting method.

4 A performance lock ends the index account option term for the index account option out of which it is transferred, effectively terminating that index account option. Once a performance lock has been processed it is irrevocable. Therefore, when a performance lock is processed, the owner will not participate in additional gains or losses their chosen index may experience.

5 The rate enhancement option can not be elected when +Income is elected. +Income and the Rate Enhancement Option are not available in New York.

6 Owners could see a substantial loss during an index period if the index declines more than the level of downside protection. If an owner does see a substantial loss during an index period, the owner may not be able to participate fully in a subsequent market recovery due to the capped upside potential in subsequent index periods.

7 Not all crediting methods and/or protection options are available with all Index Account Option terms.

8 Performance Boost is a 10% boost that is credited if the index return is flat, positive, or negative within the buffer up to the stated performance boost cap rate.

9 State variations may apply. Owners will be eligible for this waiver of withdrawal charge after the first contract anniversary. If the owner or joint owner is confined to a nursing home or hospital for 90 consecutive days by medical necessity beginning after the contract issue date, you may access up to 100% of the contract value free of withdrawal charges. All contract values will be reduced proportionately. Taxes may apply.

10 State variations may apply. Owners will be eligible for this waiver of withdrawal charge after the first contract anniversary. If the owner or joint owner is diagnosed with a terminal illness that is expected to result in death within 12 months, you may access up to 100% of the contract value free of withdrawal charges. All contract values will be reduced proportionately. Taxes may apply.

11 If the oldest owner’s age when the contract is issued is between 0 and 80, the death benefit is equal to the greater of the current contract value or premiums paid into the contract adjusted for any withdrawals incurred since the issuance of the contract. If the oldest owner’s age is between 81 and 85 when the contract is issued, the death benefit is equal to the current contract value.

12 Withdrawals during the first six premium years are subject to a withdrawal charge or market value adjustment. Withdrawals before the end of a term are subject to an interim value adjustment which may have a positive or negative impact on the contract value at the end of the term and may be significant. Market value adjustments are not applied in New York.

NASHVILLE — The Tennessee Department of Commerce & Insurance (TDCI) proudly announces that over $107 million in insurance policies and benefits was located in 2025 for Tennesseans through the Life Insurance Policy Locator Service.

Developed by the National Association of Insurance Commissioners (NAIC), the Life Insurance Policy Locator Service is a free service that enables beneficiaries, executors, or legal representatives of deceased people to locatelife insurance policies and annuity contracts of their late family members, clients, or friends.

From Jan. 1, 2025, to Dec. 31, 2025, the service located insurance policies with $107,757,080 in benefits for Tennesseans, breaking the previous record of $87.67 million set in 2024.

“I am encouraged to see that Tennesseans are claiming life insurance benefits as these policies are intended by their purchasers to help cover financial burdens such as medical bills, funeral costs, and other financial obligations that can occur after the loss of a loved one,” said TDCI Commissioner Carter Lawrence. “It is my hope that the Life Insurance Policy Locator Service eases the burden that family members and loved ones may face after the passing of a loved one, and I am grateful that the NAIC created this program.”

Looking for a deceased loved one’s lost policy? TDCI recommends that you start by reviewing financial records to see if you can find where payments have been made to an insurance company. If any of the documents reference payments made to an insurance company, you can call them directly to see if a policy can be located.

To request a search, follow these steps:

Complete NAIC’s online Life Insurance Policy Locator Service request form. Once the request is complete, NAIC will send the policyholder’s information to all licensed life insurance companies across the United States.Companies will check their records to determine if they have a policy matching the beneficiary’s information.If a match is found, the company will respond within 60 days. If a company finds a match, they will respond directly to the requestor if you are a designated beneficiary or are legally authorized to receive such information.

The service does not track beneficiary information or claim payment after matches are reported, so there is no way to determine the amount actually returned to consumers. The total claim amount only includes the amount reported by companies tied to a match for a deceased person.

For more information on the Life Insurance Policy Locator Service and other consumer insurance resources, visit our blog or contact the TDCI Consumer Insurance Service Division at 1-800-342-4029 or (615) 741-2218.

The K-shaped economy narrows in on a reality that life insurers can no longer afford to treat as secondary: Consumers are experiencing the current financial environment in very different ways, and carriers must respond accordingly.

Nick Rohan

Higher-income households may still evaluate insurance coverage through the lens of income replacement, estate planning and wealth strategy. But families on the lower half of the “K” are trying to figure out what fits into the budget now, and whether the life insurance will still be there when their family needs it. For carriers serving the middle market, or those in the $50,000 to $150,000 annual income range, this distinction should shape product strategy, distribution planning and customer engagement.

The issue becomes affordability under pressure. Inflation, elevated living costs and ongoing budget strain have made it more difficult for families to focus on protection because they’re so focused on today’s expenses. This is a call to the industry to design simpler, more flexible products, remove unnecessary friction from the buying process and build trust with consumers who are making every financial decision more carefully. Industry leaders should recognize that growth in this segment will come only from understanding how families purchase the products, not from applying traditional assumptions more aggressively.

One of the clearest takeaways for life insurance leaders is that many consumers are looking for a sustainable amount of coverage, not the perfect amount the models tell them to buy. Traditional planning models usually focus on income, debt, mortgage balances or future education costs. For households under financial strain, those calculations can quickly produce premiums that feel unrealistic. It’s the difference between recommending a plan that lasts and recommending one that lapses when it’s too expensive.

If consumers are encouraged to buy more coverage than their budgets can support, the policy may lapse, the family remains vulnerable and the insurer loses credibility. For life insurance leaders, the implication is clear: Lower face-amount products should not be treated as a compromise offering, but as an essential part of a durable protection strategy. A policy with staying power delivers more value than one that is never purchased or cannot be maintained.

Accessibility is equally important and shouldn’t be separated from affordability. Simplified products, automated underwriting and instant decisioning make it easier for consumers who may already believe life insurance is too complex or out of reach. If the experience feels slow, confusing or invasive, many consumers – especially budget-conscious ones – will walk away. Leaders should prioritize purchase journeys that are easier to understand, faster to complete and designed for follow-through.

Aiming for the middle market

Distribution strategy also must evolve. Business-to-business partnerships and public-facing platforms can help carriers reach consumers looking for smaller coverage amounts and simpler purchase paths. Many traditional carriers still do not offer products that fit this segment well or make them easy to find. Leaders should view this as a market access issue as much as a marketing issue: products built for the middle market need to be present in the channels where these consumers already make financial decisions.

Transparency plays a tremendous role as well. When budgets are tight, consumers are sensitive to anything that feels complicated or misaligned with their interests. Selling based on budget, rather than coverage amount, is a trust strategy and helps in the long term. Leaders should make clear what a policy can and cannot do, position smaller policies honestly and train teams to focus on fit and retention rather than maximum face value. At these coverage levels, small policies can prevent a family from turning to crowdfunding for funeral costs, help cover immediate expenses and create breathing room after a loss.

Trust is ultimately tested at claim time. A claims experience built around speed, automation and compassion is important for financially strained households. Fast access to funds may determine whether a family can manage funeral arrangements, cover urgent expenses or avoid deeper financial distress. In a bifurcated economy, carriers will earn trust and grow relevance by making protection reachable, understandable and dependable when it matters most.

OLDWICK, N.J.–(BUSINESS WIRE)– AM Best has assigned a Long-Term Issue Credit Rating (Long-Term IR) of “aa” (Superior) to the recently announced $1.25 billion, 6.05% surplus notes, due 2056, issued by The Northwestern Mutual Life Insurance Company (Northwestern Mutual) (Milwaukee, WI). The outlook assigned to the Credit Rating (rating) is stable.

The proceeds from the surplus notes offering will be used for general corporate purposes. The newly issued surplus notes will remain subordinated to policyowner liabilities. The company’s unadjusted financial leverage remains low at 20% with favorable interest coverage over 3x post policyholder dividends, as calculated by AM Best, which is considered within guidelines for the assigned rating. Northwestern Mutual’s existing ratings continue to reflect its balance sheet strength, which AM Best assesses as strongest, as well as its very strong operating performance, very favorable business profile and very strong enterprise risk management.

This press release relates to Credit Ratings that have been published on AM Best’s website. For all rating information relating to the release and pertinent disclosures, including details of the office responsible for issuing each of the individual ratings referenced in this release, please see AM Best’s Recent Rating Activity web page. For additional information regarding the use and limitations of Credit Rating opinions, please view Guide to Best’s Credit Ratings. For information on the proper use of Best’s Credit Ratings, Best’s Performance Assessments, Best’s Preliminary Credit Assessments and AM Best press releases, please view Guide to Proper Use of Best’s Ratings & Assessments.

AM Best is a global credit rating agency, news publisher and data analytics provider specializing in the insurance industry. Headquartered in the United States, the company does business in over 100 countries with regional offices in London, Amsterdam, Dubai, Hong Kong, Singapore and Mexico City. For more information, visit www.ambest.com.

OLDWICK, N.J.–(BUSINESS WIRE)– AM Best has affirmed the Financial Strength Rating (FSR) of A (Excellent) and the Long-Term Issuer Credit Ratings (Long-Term ICR) of “a” (Excellent) of Aetna Life Insurance Company (ALIC) (Hartford, CT) and the other members of Aetna Health & Life Group, which are operating entities of Aetna Inc. (Aetna) and wholly owned subsidiaries of its ultimate parent, CVS Health Corporation (CVS Health) (NYSE: CVS). (Please see below for a detailed listing of the companies.)

Concurrently, AM Best has affirmed the FSR of A (Excellent) and the Long-Term ICR of “a” (Excellent) of Allina Health and Aetna Insurance Company (Allina Health) (St. Louis Park, MN). Allina Health is a joint venture subsidiary of Aetna.

AM Best also has affirmed the FSR of A (Excellent) and the Long-Term ICR of “a” (Excellent) of CVS Caremark Indemnity Ltd. (CVS Caremark Indemnity) (Bermuda). The outlook of all these Credit Ratings (ratings) is stable.

The ratings of Aetna Health & Life Group reflect its balance sheet strength, which AM Best assesses as very strong, as well as its strong operating performance, favorable business profile and appropriate enterprise risk management (ERM).

Aetna Health & Life Group’s rating affirmations also reflects its strongest level of risk-adjusted capitalization, as measured by Best Capital Adequacy Ratio (BCAR). While historically the group has paid large dividends to its parents while maintaining the strongest levels of risk-adjusted capitalization, this trend reversed in 2024 when CVS Health contributed capital to support losses and growth in the business. Capital improved in 2025, driven by earnings; however, AM Best notes that dividends paid to the parent were lower than normal and are expected to return to historical levels in the near term. Investments remain managed centrally at the enterprise level, and the risk profile of the group’s investment portfolio has remained consistent over the last few years, although there has been steady increases in schedule BA assets. Aetna Health & Life Group’s investment portfolio primarily holds investment-grade fixed-income securities, schedule BA assets, as well as cash and cash equivalents.

Aetna Health & Life Group’s balance sheet strength is also supported by adequate liquidity measures, which are further supported by access to the Federal Home Loan Bank of Boston at the lead entity, Aetna Life Insurance Company. Aetna Health & Life Group continues to have moderate reinsurance leverage; although, its reinsurance arrangements differentiate Aetna from its health insurance peers. In addition to traditional reinsurance with highly rated carriers, Aetna Health & Life Group maintains a quota share reinsurance agreement with Health Re, Inc. and subsequent excess of loss protection by Vitality Re entities, which had another issuance in 2026, expiring in 2030.

In 2025, net premium written growth was driven by a strong increase in government programs mainly driven by changes to Medicare Part D from the Inflation Reduction Act, rating actions, partially offset by declining memberships driven primarily by the group’s repricing strategy.

Underwriting and net earnings improved in 2025, driven by an improvement in Medicare Advantage Star Ratings for its Medicare Advantage plans, with 88% of members in a four + star rated plan, along with initiatives taken to improve profitability. This follows a challenging year in 2024, when underwriting losses were driven by several factors including: increased utilization, the unfavorable impact of the decline in the group’s Medicare Advantage Star Ratings for the 2024 payment year, as well as higher acuity in Medicaid. Additionally, investment income has been steady over the last five years and is expected to continue to be accretive to earnings.

Aetna is one of the nation’s leading providers of employee health insurance benefits. Aetna’s lines of business are diversified by both product and geography. Furthermore, Aetna maintains a strong market position in the Medicare, Medicaid and commercial market and competes in all U.S. states. AM Best notes that Aetna exited the individual ACA market effective January 1, 2026.

The ratings of Aetna Health & Life Group reflect the negative impact from CVS Health, which has elevated financial leverage and goodwill. Unfavorable underwriting performance in 2024 resulted in capital contributions from CVS Health to its insurance subsidiaries, contributing to elevated leverage at the parent. Financial leverage declined slightly in 2025, due to slightly lower debt outstanding and improved earnings. Goodwill and intangibles-to-shareholders equity improved in 2025, driven by lower goodwill due to the goodwill impairment charge related to CVS Health’s Health Care Delivery reporting unit that occurred in third-quarter 2025 for Oak Street Health. However, the goodwill and intangibles to equity still exceeded 130% at year-end 2025.

The ratings reflect Allina Health’s balance sheet strength, which AM Best assesses as adequate, as well as its marginal operating performance, limited business profile and appropriate ERM and the support of the Aetna organization. Allina Health has reported net and underwriting losses for the last two years. While Allina Health reported an underwriting loss in 2025, it marked an improvement compared to the prior year. The improvement was mainly driven by lower-than expected medical costs in the Medicare Advantage. Over the last few years, the company has reported net losses due to the amortization of intangible assets, which is expected to end in 2026. After this, net income is expected to improve in future years.

The ratings reflect CVS Caremark Indemnity’s balance sheet strength, which AM Best assesses as very strong, as well as its adequate operating performance, neutral business profile and appropriate ERM and the support of its parent. The company’s market position is largely dependent on CVS Health, as all of the business CVS Caremark Indemnity writes or assumes involves CVS Health affiliated entities. Most importantly, the company has a 15% quota share agreement with SilverScript Insurance Company, a CVS Health affiliate, which comprises most of its premiums.

The FSR of A (Excellent) and the Long-Term ICRs of “a” (Excellent) have been affirmed, with stable outlooks for the following members of Aetna Health & Life Group:

Aetna Life Insurance Company

Aetna Health and Life Insurance Company

Aetna Life & Casualty (Bermuda) Ltd.

Aetna Health Inc. (a Connecticut corporation)

Aetna Health Inc. (a Florida corporation)

Aetna Health Inc. (a Georgia corporation)

Aetna Health Inc. (a Louisiana corporation)

Aetna Health Inc. (a New Jersey corporation)

Aetna Health Inc. (a New York corporation)

Aetna Health Inc. (a Maine Corporation)

Aetna Health Inc. (a Pennsylvania corporation)

Aetna Health Inc. (a Texas corporation)

Aetna Health Insurance Company

Aetna Health Insurance Company of New York

Aetna Better Health of Florida, Inc.

Aetna Health of California Inc.

Aetna Health of Iowa, Inc.

Aetna Health of Utah, Inc.

Aetna Dental of California Inc.

Aetna Dental Inc. (a New Jersey corporation)

Aetna Dental Inc. (a Texas corporation)

American Continental Insurance Company

Accendo Insurance Company

Continental Life Insurance Company of Brentwood, Tennessee

Coventry Health and Life Insurance Company

Aetna Better Health of Michigan, Inc.

Aetna Better Health of Missouri, LLC

Coventry Health Care of Illinois, Inc.

Coventry Health Care of Kansas, Inc.

Coventry Health Care of Missouri, Inc.

Coventry Health Care of Nebraska, Inc.

Coventry Health Care of Virginia, Inc.

Coventry Health Care of West Virginia, Inc.

First Health Life & Health Insurance Company

SilverScript Insurance Company

This press release relates to Credit Ratings that have been published on AM Best’s website. For all rating information relating to the release and pertinent disclosures, including details of the office responsible for issuing each of the individual ratings referenced in this release, please see AM Best’s Recent Rating Activity web page. For additional information regarding the use and limitations of Credit Rating opinions, please view Guide to Best’s Credit Ratings. For information on the proper use of Best’s Credit Ratings, Best’s Performance Assessments, Best’s Preliminary Credit Assessments and AM Best press releases, please view Guide to Proper Use of Best’s Ratings & Assessments.

AM Best is a global credit rating agency, news publisher and data analytics provider specializing in the insurance industry. Headquartered in the United States, the company does business in over 100 countries with regional offices in London, Amsterdam, Dubai, Hong Kong, Singapore and Mexico City. For more information, visit www.ambest.com.

Prudential Financial is undergoing another round of layoffs as the company continues to evolve in Year Two under CEO Andrew Sullivan.

According to a filing with the New Jersey Department of Labor and Workforce Development, Prudential is laying off 53 employees on July 17. That follows previous layoff notices in March (54 employees), November (63), September (63) and July 2025 (57).

Sullivan officially succeeded Charles F. Lowrey on March 31, 2025.

A spokesperson for Prudential pointed out that the Newark, N.J.-based insurer is a worldwide company with 36,000 employees.

“Prudential is strengthening our business to deliver long-term growth by investing in the capabilities where we’re most competitive,” reads a statement from Prudential. “That means continually making targeted adjustments including, at times, reorganizing our workforce to align with the company’s strategy. These decisions are never easy, and we’re committed to providing impacted employees with support, care and respect.”

Japan problems

Prudential executives are dealing with an earnings drag due to problems in its Japan affiliate. Prudential of Japan is currently navigating severe compliance issues involving employee misconduct and inappropriate investment solicitations, resulting in a prolonged halt on new sales.

Prudential initiated a voluntary 90-day suspension of new POJ sales in February 2026. The sales pause was extended for an additional 180 days after it was determined the Japanese subsidiary was not ready to resume operations, extending the suspension through late 2026.

The total revenue loss and remediation cost associated with the Japanese market disruptions is estimated at approximately $1 billion.

Overhauling the team

Prudential overhauled its leadership team, restructured operations, and shed noncore assets to fuel growth in retirement and asset management, explained Sullivan and Yanela Frias, executive vice president and chief financial officer, during the company’s recent Q1 2026 earnings call.

The company had higher operating expenses, Frias said, but is investing in service and technology to offer an “enhanced customer experience.” Prudential expects to see expense savings show up in 2027, she added during the May call.

“These are investments in things like modernizing and driving efficiencies in onboarding and claims management and group, and investments in service delivery throughout all our U.S. businesses,” Frias said. “These do lead to efficiencies.”

Prudential entered 2026 with a realignment of its senior business leadership structure. As a result, leaders responsible for the company’s U.S. businesses, Emerging Markets, the Japan Group and Prudential’s asset management business, PGIM, now report directly to Sullivan.

Phil Waldeck was appointed executive vice president, head of Prudential’s U.S. Businesses. In a corresponding move, Caroline Feeney, global head of Retirement and Insurance, departed Prudential after a 33-year career with the insurer.

NASHVILLE — The Tennessee Department of Commerce & Insurance (TDCI) proudly announces that over $107 million in insurance policies and benefits was located in 2025 for Tennesseans through the Life Insurance Policy Locator Service.

Developed by the National Association of Insurance Commissioners (NAIC), the Life Insurance Policy Locator Service is a free service that enables beneficiaries, executors, or legal representatives of deceased people to locate life insurance policies and annuity contracts of their late family members, clients, or friends.

From Jan. 1, 2025, to Dec. 31, 2025, the service located insurance policies with $107,757,080 in benefits for Tennesseans, breaking the previous record of $87.67 million set in 2024.

“I am encouraged to see that Tennesseans are claiming life insurance benefits as these policies are intended by their purchasers to help cover financial burdens such as medical bills, funeral costs, and other financial obligations that can occur after the loss of a loved one,” said TDCI Commissioner Carter Lawrence.

“It is my hope that the Life Insurance Policy Locator Service eases the burden that family members and loved ones may face after the passing of a loved one, and I am grateful that the NAIC created this program.”

Looking for a deceased loved one’s lost policy? TDCI recommends that you start by reviewing financial records to see if you can find where payments have been made to an insurance company. If any of the documents reference payments made to an insurance company, you can call them directly to see if a policy can be located.

To request a search, follow these steps:

Complete NAIC’s online Life Insurance Policy Locator Service request form. Once the request is complete, NAIC will send the policyholder’s information to all licensed life insurance companies across the United States.

Companies will check their records to determine if they have a policy matching the beneficiary’s information.

If a match is found, the company will respond within 60 days. If a company finds a match, they will respond directly to the requestor if you are a designated beneficiary or are legally authorized to receive such information.

The service does not track beneficiary information or claim payment after matches are reported, so there is no way to determine the amount actually returned to consumers. The total claim amount only includes the amount reported by companies tied to a match for a deceased person.

For more information on the Life Insurance Policy Locator Service and other consumer insurance resources, visit our blog or contact the TDCI Consumer Insurance Service Division at 1-800-342-4029 or (615) 741-2218.

, The 500

, The 500